User login

Our specialty sees contraception as a basic element of women’s preventive care. It helps women determine and space their pregnancies; helps ensure healthier pregnancies; and helps many women with health-care concerns not related to pregnancy to better manage their symptoms and stay healthy.

The drafters of the Affordable Care Act (ACA) recognized the importance of contraception to women’s health when they guaranteed coverage of prescription contraceptives and services, including all methods approved by the US Food and Drug Administration, without deductibles or copays, to millions of women through their private health insurance. This policy was vetted and approved by the Institute of Medicine (IOM) and US Department of Health and Human Services (HHS).

The American Congress of Obstetricians and Gynecologists (ACOG) was central to these discussions. ACOG Executive Vice President and CEO Hal C. Lawrence III, MD, offered our women’s health guidelines and guidance to the IOM, the entity designated by the Secretary of HHS to recommend exactly what coverage and services should fall within the category of women’s preventive care. ACOG’s recommendations were broadly accepted by IOM and HHS and are now required coverage for women across the nation.

Related Article: ACOG to legislators: Partnership, not interference Lucia DiVenere, MA (April 2013)

So, why the confusion and controversy?

Let’s clear up the confusion first.

We’ve heard that private health plans now are required to cover contraceptives without cost sharing. But it’s a little more complicated than that.

CONTRACEPTIVE MANDATE AFFECTS NEW PLANS ONLY

It’s true that the ACA requires new private plans to cover a broad range of preventive services:

- evidence-based screenings and counseling

- routine immunizations

- childhood preventive services

- preventive services for women.

Did you catch the word “new” in that sentence?

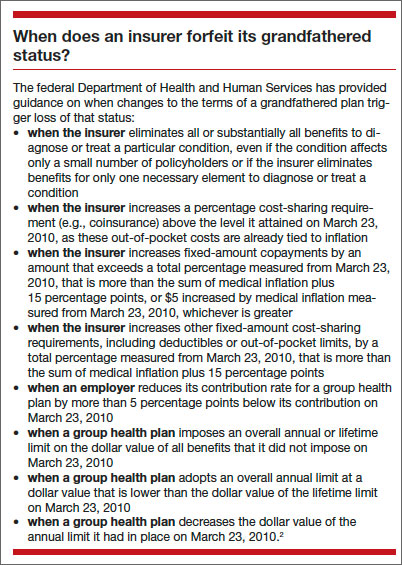

Health plans that existed before March 23, 2010—the date the ACA was signed into law—and that haven’t changed in ways that substantially cut benefits or increase costs for consumers are considered “grandfathered plans” and are not required to abide by these and other requirements in the law.

There are two types of grandfathered plans:

- job-based plans—health insurance plans administered through employers can continue to enroll people as long as no significant changes are made to coverage

- individual plans—a grandfathered plan purchased by an individual cannot expand coverage beyond that individual.

Any insurer can cancel a grandfathered plan as long as it provides 90-day notice to the plan’s enrollees and offers other coverage options. Because grandfathered plans are exempt from a number of ACA benefits and protections, these plans are required to disclose their status to their enrollees.

The number of people enrolled in grandfathered plans is steadily decreasing. In 2013, 36% of people covered through their jobs were enrolled in a grandfathered health plan, down from 48% in 2012 and 56% in 2011, according to the Kaiser Family Foundation.1 Here’s a quick look at the consumer protections that do and do not apply to grandfathered plans.

All health plans must:

- end lifetime limits on coverage

- end arbitrary cancellations of health coverage

- cover adult children up to age 26

- provide a Summary of Benefits and Coverage, a short, easy-to-understand summary of what a plan covers and costs

- spend revenue from premiums on health care, not on administrative costs and bonuses.

Grandfathered plans don’t have to:

- cover preventive care for free, including contraceptives

- guarantee your right to appeal

- protect your choice of doctors and access to emergency care

- be held accountable through Rate Review for excessive premium increases.

Nor do grandfathered individual plans (the kind you buy yourself, not the kind you get from an employer) have to end yearly limits on coverage or cover a preexisting health condition.

Right away, then, we have a situation in which some patients may have 100% coverage for contraceptives while others don’t, especially if their plans were in effect before the ACA became law.

Nonprofits with religious ties are exempted, too

There’s a second segment of your patient population that may not have full contraceptive coverage: those who are covered through employment with a religiously affiliated nonprofit. Initially, in August 2011, only health insurance provided through employment with houses of worship was exempted from the requirement to cover contraceptives. In July 2013, this exemption was expanded to address concerns from other religious affiliates, including universities and hospitals.

This “accommodation,” as it’s known, exempts religiously affiliated nonprofits with religious objections from contracting, arranging, paying for, or referring for contraceptive coverage for their employees. Instead, their insurers are required to provide this coverage free of charge to the employer or employees—an attempt to ensure that all women have the same access to care, regardless of their employment setting. This accommodation is available only to organizations that:

- oppose the mandate to provide contraceptive coverage because of religious beliefs

- are nonprofit

- hold themselves out as religious organizations AND

- self-certify that they meet the just-stated requirements of 1–3.

Related article: As the Affordable Care Act comes of age, a look behind the headlines Lucia DiVenere, MA (January 2014)

The rule for small companies

There’s a third group that doesn’t have to provide contraceptive coverage to employees: for-profit companies with fewer than 50 workers. Under the law, these employers have two options:

- Provide no health care: This option carries no penalty but, rather, is an attempt to help small businesses, now that individuals can buy coverage on the exchanges

- Offer health care: If small businesses choose this option, their coverage must include contraceptive care.

So when your patient approaches your front desk to pay her bill, or picks up her contraceptive prescription at the pharmacy, her bill will vary, depending on the age of her plan, her employer’s religious status, and the size of the business she works for. It’s important that you check her coverage with her policy.

Now, on to the controversy.

FOR-PROFIT COMPANIES ALSO SEEK EXEMPTION

Houses of worship are exempted and religiously affiliated nonprofit organizations are offered an accommodation to avoid direct involvement with the contraceptive coverage mandate. More than 40 religiously affiliated nonprofit corporations are currently challenging the mandate, asserting that the accommodation still burdens their religious rights.

What happens when owners of a for-profit corporation claim a religious right to not offer contraceptive coverage to their employees? That’s the question currently before the US Supreme Court. As of this writing, the Court heard arguments on March 25, 2014, and is likely to hand down its decision in two cases in June. The two corporations involved are Conestoga Wood Specialties and Hobby Lobby Stores.

Under the ACA, for-profit employers do not qualify for religious exemptions or accommodations from the contraceptive coverage mandate. As we saw earlier, the mandate varies in its application to these employers by employer size. All for-profit employers with 50 or more employees must provide coverage, unless their coverage is through a grandfathered plan. Employers with fewer than 50 workers have two options. They’re not penalized if they don’t offer any health-care coverage to their employees—but if they do, that coverage must include contraception.

Both Conestoga and Hobby Lobby are major employers. Conestoga Wood has 950 full-time employees. Hobby Lobby operates 514 stores in 41 states, with more than 13,000 employees.

Lower court rulings have been conflicting

The Supreme Court agreed to review and rule on these cases largely to settle widely divergent rulings at lower court levels. As of this writing, more than 40 for-profit businesses have challenged the coverage mandate in federal court. The Conestoga and Hobby Lobby owners, like the owners of other businesses challenging the law, say that because they are religious families—Mennonite and Protestant, respectively—and they run their businesses according to their faiths, their religious views extend to their businesses. They claim that the ACA mandate violates their First Amendment right to protection of free exercise of religion as well as their rights under the 1993 Religious Freedom Restoration Act (RFRA), a law enacted to protect individuals from laws that substantially burden their exercise of religion. They are left, they assert, with a choice of providing objectionable coverage or paying a fine, a substantial burden on their freedom of religion.

The key issue before the Court is whether secular for-profit corporations can avoid complying with the legal mandates of the ACA based on the religious beliefs of their owners. To date, five federal circuit courts have ruled on the RFRA claim. Some have determined that corporations have no religious rights. Others have found the opposite. The Supreme Court will attempt to set the path for lower courts to follow.

The outcome of these cases will have a profound effect on women’s health, and may be felt much more broadly in our health-care system. If a business owner can opt out of one sort of coverage based on his or her religious beliefs, then wouldn’t that rule apply to other areas of health care? Employers might choose not to cover childhood immunizations, blood transfusions, or maternity care for single workers. Allowing employers to pick and choose can be risky business.

ACOG joins an amicus brief

ACOG partnered with a number of other preeminent health-care organizations, including the American Academy of Pediatrics, the American College of Nurse-Midwives, the American Society for Reproductive Medicine, the Society for Maternal-Fetal Medicine, Physicians for Reproductive Health, and the International Association of Forensic Nurses, to prepare an amicus brief to the Court on these cases.

The arguments we and our colleagues put forward centered on two points:

- Employers should not be allowed to interfere in the provider-patient relationship

- Allowing employers to veto coverage based on their own religious beliefs has broad and troubling public health implications.

Contraception is an essential component of women’s health care. The Supreme Court could unravel this important new guarantee or protect it for today’s and future generations.

Acknowledgment

The author thanks and acknowledges Sara Needleman Kline, JD, Deputy General Counsel, ACOG, for her helpful review and comments.

WE WANT TO HEAR FROM YOU!

Share your thoughts on this article or on any topic relevant to ObGyns and women’s health practitioners. Tell us which topics you’d like to see covered in future issues, and what challenges you face in daily practice. We will consider publishing your letter in a future issue. Send your letter to: obg@frontlinemedcom.com Please include the city and state in which you practice. Stay in touch! Your feedback is important to us!

- Kaiser Family Foundation. 2013 Employer Health Benefits Survey. http://kff.org/private-insurance/report/2013-employer-health-benefits/. Published August 20, 2013. Accessed March 27, 2014.

- Office of the US Federal Register. Definition of Grandfathered Health Plan Coverage in Paragraph (a) of 26 CFR 54.9815-1251T, 29 CFR 2590.715-1251, and 45 CFR 147.140 of These Interim Final Regulations. https://www.federalregister.gov/articles/2010/06/17/2010-14488/interim-final-rules-for-group-health-plans-and-health-insurance-coverage-relating-to-status-as-a#h-11. Published June 17, 2010. Accessed March 25, 2014.

Lucia DiVenere, MA, is Officer, Government and Political Affairs at the American Congress of Obstetricians and Gynecologists, Washington, DC.

The author reports no financial relationships relevant to this article.

Lucia DiVenere, MA, is Officer, Government and Political Affairs at the American Congress of Obstetricians and Gynecologists, Washington, DC.

The author reports no financial relationships relevant to this article.

Lucia DiVenere, MA, is Officer, Government and Political Affairs at the American Congress of Obstetricians and Gynecologists, Washington, DC.

The author reports no financial relationships relevant to this article.

Our specialty sees contraception as a basic element of women’s preventive care. It helps women determine and space their pregnancies; helps ensure healthier pregnancies; and helps many women with health-care concerns not related to pregnancy to better manage their symptoms and stay healthy.

The drafters of the Affordable Care Act (ACA) recognized the importance of contraception to women’s health when they guaranteed coverage of prescription contraceptives and services, including all methods approved by the US Food and Drug Administration, without deductibles or copays, to millions of women through their private health insurance. This policy was vetted and approved by the Institute of Medicine (IOM) and US Department of Health and Human Services (HHS).

The American Congress of Obstetricians and Gynecologists (ACOG) was central to these discussions. ACOG Executive Vice President and CEO Hal C. Lawrence III, MD, offered our women’s health guidelines and guidance to the IOM, the entity designated by the Secretary of HHS to recommend exactly what coverage and services should fall within the category of women’s preventive care. ACOG’s recommendations were broadly accepted by IOM and HHS and are now required coverage for women across the nation.

Related Article: ACOG to legislators: Partnership, not interference Lucia DiVenere, MA (April 2013)

So, why the confusion and controversy?

Let’s clear up the confusion first.

We’ve heard that private health plans now are required to cover contraceptives without cost sharing. But it’s a little more complicated than that.

CONTRACEPTIVE MANDATE AFFECTS NEW PLANS ONLY

It’s true that the ACA requires new private plans to cover a broad range of preventive services:

- evidence-based screenings and counseling

- routine immunizations

- childhood preventive services

- preventive services for women.

Did you catch the word “new” in that sentence?

Health plans that existed before March 23, 2010—the date the ACA was signed into law—and that haven’t changed in ways that substantially cut benefits or increase costs for consumers are considered “grandfathered plans” and are not required to abide by these and other requirements in the law.

There are two types of grandfathered plans:

- job-based plans—health insurance plans administered through employers can continue to enroll people as long as no significant changes are made to coverage

- individual plans—a grandfathered plan purchased by an individual cannot expand coverage beyond that individual.

Any insurer can cancel a grandfathered plan as long as it provides 90-day notice to the plan’s enrollees and offers other coverage options. Because grandfathered plans are exempt from a number of ACA benefits and protections, these plans are required to disclose their status to their enrollees.

The number of people enrolled in grandfathered plans is steadily decreasing. In 2013, 36% of people covered through their jobs were enrolled in a grandfathered health plan, down from 48% in 2012 and 56% in 2011, according to the Kaiser Family Foundation.1 Here’s a quick look at the consumer protections that do and do not apply to grandfathered plans.

All health plans must:

- end lifetime limits on coverage

- end arbitrary cancellations of health coverage

- cover adult children up to age 26

- provide a Summary of Benefits and Coverage, a short, easy-to-understand summary of what a plan covers and costs

- spend revenue from premiums on health care, not on administrative costs and bonuses.

Grandfathered plans don’t have to:

- cover preventive care for free, including contraceptives

- guarantee your right to appeal

- protect your choice of doctors and access to emergency care

- be held accountable through Rate Review for excessive premium increases.

Nor do grandfathered individual plans (the kind you buy yourself, not the kind you get from an employer) have to end yearly limits on coverage or cover a preexisting health condition.

Right away, then, we have a situation in which some patients may have 100% coverage for contraceptives while others don’t, especially if their plans were in effect before the ACA became law.

Nonprofits with religious ties are exempted, too

There’s a second segment of your patient population that may not have full contraceptive coverage: those who are covered through employment with a religiously affiliated nonprofit. Initially, in August 2011, only health insurance provided through employment with houses of worship was exempted from the requirement to cover contraceptives. In July 2013, this exemption was expanded to address concerns from other religious affiliates, including universities and hospitals.

This “accommodation,” as it’s known, exempts religiously affiliated nonprofits with religious objections from contracting, arranging, paying for, or referring for contraceptive coverage for their employees. Instead, their insurers are required to provide this coverage free of charge to the employer or employees—an attempt to ensure that all women have the same access to care, regardless of their employment setting. This accommodation is available only to organizations that:

- oppose the mandate to provide contraceptive coverage because of religious beliefs

- are nonprofit

- hold themselves out as religious organizations AND

- self-certify that they meet the just-stated requirements of 1–3.

Related article: As the Affordable Care Act comes of age, a look behind the headlines Lucia DiVenere, MA (January 2014)

The rule for small companies

There’s a third group that doesn’t have to provide contraceptive coverage to employees: for-profit companies with fewer than 50 workers. Under the law, these employers have two options:

- Provide no health care: This option carries no penalty but, rather, is an attempt to help small businesses, now that individuals can buy coverage on the exchanges

- Offer health care: If small businesses choose this option, their coverage must include contraceptive care.

So when your patient approaches your front desk to pay her bill, or picks up her contraceptive prescription at the pharmacy, her bill will vary, depending on the age of her plan, her employer’s religious status, and the size of the business she works for. It’s important that you check her coverage with her policy.

Now, on to the controversy.

FOR-PROFIT COMPANIES ALSO SEEK EXEMPTION

Houses of worship are exempted and religiously affiliated nonprofit organizations are offered an accommodation to avoid direct involvement with the contraceptive coverage mandate. More than 40 religiously affiliated nonprofit corporations are currently challenging the mandate, asserting that the accommodation still burdens their religious rights.

What happens when owners of a for-profit corporation claim a religious right to not offer contraceptive coverage to their employees? That’s the question currently before the US Supreme Court. As of this writing, the Court heard arguments on March 25, 2014, and is likely to hand down its decision in two cases in June. The two corporations involved are Conestoga Wood Specialties and Hobby Lobby Stores.

Under the ACA, for-profit employers do not qualify for religious exemptions or accommodations from the contraceptive coverage mandate. As we saw earlier, the mandate varies in its application to these employers by employer size. All for-profit employers with 50 or more employees must provide coverage, unless their coverage is through a grandfathered plan. Employers with fewer than 50 workers have two options. They’re not penalized if they don’t offer any health-care coverage to their employees—but if they do, that coverage must include contraception.

Both Conestoga and Hobby Lobby are major employers. Conestoga Wood has 950 full-time employees. Hobby Lobby operates 514 stores in 41 states, with more than 13,000 employees.

Lower court rulings have been conflicting

The Supreme Court agreed to review and rule on these cases largely to settle widely divergent rulings at lower court levels. As of this writing, more than 40 for-profit businesses have challenged the coverage mandate in federal court. The Conestoga and Hobby Lobby owners, like the owners of other businesses challenging the law, say that because they are religious families—Mennonite and Protestant, respectively—and they run their businesses according to their faiths, their religious views extend to their businesses. They claim that the ACA mandate violates their First Amendment right to protection of free exercise of religion as well as their rights under the 1993 Religious Freedom Restoration Act (RFRA), a law enacted to protect individuals from laws that substantially burden their exercise of religion. They are left, they assert, with a choice of providing objectionable coverage or paying a fine, a substantial burden on their freedom of religion.

The key issue before the Court is whether secular for-profit corporations can avoid complying with the legal mandates of the ACA based on the religious beliefs of their owners. To date, five federal circuit courts have ruled on the RFRA claim. Some have determined that corporations have no religious rights. Others have found the opposite. The Supreme Court will attempt to set the path for lower courts to follow.

The outcome of these cases will have a profound effect on women’s health, and may be felt much more broadly in our health-care system. If a business owner can opt out of one sort of coverage based on his or her religious beliefs, then wouldn’t that rule apply to other areas of health care? Employers might choose not to cover childhood immunizations, blood transfusions, or maternity care for single workers. Allowing employers to pick and choose can be risky business.

ACOG joins an amicus brief

ACOG partnered with a number of other preeminent health-care organizations, including the American Academy of Pediatrics, the American College of Nurse-Midwives, the American Society for Reproductive Medicine, the Society for Maternal-Fetal Medicine, Physicians for Reproductive Health, and the International Association of Forensic Nurses, to prepare an amicus brief to the Court on these cases.

The arguments we and our colleagues put forward centered on two points:

- Employers should not be allowed to interfere in the provider-patient relationship

- Allowing employers to veto coverage based on their own religious beliefs has broad and troubling public health implications.

Contraception is an essential component of women’s health care. The Supreme Court could unravel this important new guarantee or protect it for today’s and future generations.

Acknowledgment

The author thanks and acknowledges Sara Needleman Kline, JD, Deputy General Counsel, ACOG, for her helpful review and comments.

WE WANT TO HEAR FROM YOU!

Share your thoughts on this article or on any topic relevant to ObGyns and women’s health practitioners. Tell us which topics you’d like to see covered in future issues, and what challenges you face in daily practice. We will consider publishing your letter in a future issue. Send your letter to: obg@frontlinemedcom.com Please include the city and state in which you practice. Stay in touch! Your feedback is important to us!

Our specialty sees contraception as a basic element of women’s preventive care. It helps women determine and space their pregnancies; helps ensure healthier pregnancies; and helps many women with health-care concerns not related to pregnancy to better manage their symptoms and stay healthy.

The drafters of the Affordable Care Act (ACA) recognized the importance of contraception to women’s health when they guaranteed coverage of prescription contraceptives and services, including all methods approved by the US Food and Drug Administration, without deductibles or copays, to millions of women through their private health insurance. This policy was vetted and approved by the Institute of Medicine (IOM) and US Department of Health and Human Services (HHS).

The American Congress of Obstetricians and Gynecologists (ACOG) was central to these discussions. ACOG Executive Vice President and CEO Hal C. Lawrence III, MD, offered our women’s health guidelines and guidance to the IOM, the entity designated by the Secretary of HHS to recommend exactly what coverage and services should fall within the category of women’s preventive care. ACOG’s recommendations were broadly accepted by IOM and HHS and are now required coverage for women across the nation.

Related Article: ACOG to legislators: Partnership, not interference Lucia DiVenere, MA (April 2013)

So, why the confusion and controversy?

Let’s clear up the confusion first.

We’ve heard that private health plans now are required to cover contraceptives without cost sharing. But it’s a little more complicated than that.

CONTRACEPTIVE MANDATE AFFECTS NEW PLANS ONLY

It’s true that the ACA requires new private plans to cover a broad range of preventive services:

- evidence-based screenings and counseling

- routine immunizations

- childhood preventive services

- preventive services for women.

Did you catch the word “new” in that sentence?

Health plans that existed before March 23, 2010—the date the ACA was signed into law—and that haven’t changed in ways that substantially cut benefits or increase costs for consumers are considered “grandfathered plans” and are not required to abide by these and other requirements in the law.

There are two types of grandfathered plans:

- job-based plans—health insurance plans administered through employers can continue to enroll people as long as no significant changes are made to coverage

- individual plans—a grandfathered plan purchased by an individual cannot expand coverage beyond that individual.

Any insurer can cancel a grandfathered plan as long as it provides 90-day notice to the plan’s enrollees and offers other coverage options. Because grandfathered plans are exempt from a number of ACA benefits and protections, these plans are required to disclose their status to their enrollees.

The number of people enrolled in grandfathered plans is steadily decreasing. In 2013, 36% of people covered through their jobs were enrolled in a grandfathered health plan, down from 48% in 2012 and 56% in 2011, according to the Kaiser Family Foundation.1 Here’s a quick look at the consumer protections that do and do not apply to grandfathered plans.

All health plans must:

- end lifetime limits on coverage

- end arbitrary cancellations of health coverage

- cover adult children up to age 26

- provide a Summary of Benefits and Coverage, a short, easy-to-understand summary of what a plan covers and costs

- spend revenue from premiums on health care, not on administrative costs and bonuses.

Grandfathered plans don’t have to:

- cover preventive care for free, including contraceptives

- guarantee your right to appeal

- protect your choice of doctors and access to emergency care

- be held accountable through Rate Review for excessive premium increases.

Nor do grandfathered individual plans (the kind you buy yourself, not the kind you get from an employer) have to end yearly limits on coverage or cover a preexisting health condition.

Right away, then, we have a situation in which some patients may have 100% coverage for contraceptives while others don’t, especially if their plans were in effect before the ACA became law.

Nonprofits with religious ties are exempted, too

There’s a second segment of your patient population that may not have full contraceptive coverage: those who are covered through employment with a religiously affiliated nonprofit. Initially, in August 2011, only health insurance provided through employment with houses of worship was exempted from the requirement to cover contraceptives. In July 2013, this exemption was expanded to address concerns from other religious affiliates, including universities and hospitals.

This “accommodation,” as it’s known, exempts religiously affiliated nonprofits with religious objections from contracting, arranging, paying for, or referring for contraceptive coverage for their employees. Instead, their insurers are required to provide this coverage free of charge to the employer or employees—an attempt to ensure that all women have the same access to care, regardless of their employment setting. This accommodation is available only to organizations that:

- oppose the mandate to provide contraceptive coverage because of religious beliefs

- are nonprofit

- hold themselves out as religious organizations AND

- self-certify that they meet the just-stated requirements of 1–3.

Related article: As the Affordable Care Act comes of age, a look behind the headlines Lucia DiVenere, MA (January 2014)

The rule for small companies

There’s a third group that doesn’t have to provide contraceptive coverage to employees: for-profit companies with fewer than 50 workers. Under the law, these employers have two options:

- Provide no health care: This option carries no penalty but, rather, is an attempt to help small businesses, now that individuals can buy coverage on the exchanges

- Offer health care: If small businesses choose this option, their coverage must include contraceptive care.

So when your patient approaches your front desk to pay her bill, or picks up her contraceptive prescription at the pharmacy, her bill will vary, depending on the age of her plan, her employer’s religious status, and the size of the business she works for. It’s important that you check her coverage with her policy.

Now, on to the controversy.

FOR-PROFIT COMPANIES ALSO SEEK EXEMPTION

Houses of worship are exempted and religiously affiliated nonprofit organizations are offered an accommodation to avoid direct involvement with the contraceptive coverage mandate. More than 40 religiously affiliated nonprofit corporations are currently challenging the mandate, asserting that the accommodation still burdens their religious rights.

What happens when owners of a for-profit corporation claim a religious right to not offer contraceptive coverage to their employees? That’s the question currently before the US Supreme Court. As of this writing, the Court heard arguments on March 25, 2014, and is likely to hand down its decision in two cases in June. The two corporations involved are Conestoga Wood Specialties and Hobby Lobby Stores.

Under the ACA, for-profit employers do not qualify for religious exemptions or accommodations from the contraceptive coverage mandate. As we saw earlier, the mandate varies in its application to these employers by employer size. All for-profit employers with 50 or more employees must provide coverage, unless their coverage is through a grandfathered plan. Employers with fewer than 50 workers have two options. They’re not penalized if they don’t offer any health-care coverage to their employees—but if they do, that coverage must include contraception.

Both Conestoga and Hobby Lobby are major employers. Conestoga Wood has 950 full-time employees. Hobby Lobby operates 514 stores in 41 states, with more than 13,000 employees.

Lower court rulings have been conflicting

The Supreme Court agreed to review and rule on these cases largely to settle widely divergent rulings at lower court levels. As of this writing, more than 40 for-profit businesses have challenged the coverage mandate in federal court. The Conestoga and Hobby Lobby owners, like the owners of other businesses challenging the law, say that because they are religious families—Mennonite and Protestant, respectively—and they run their businesses according to their faiths, their religious views extend to their businesses. They claim that the ACA mandate violates their First Amendment right to protection of free exercise of religion as well as their rights under the 1993 Religious Freedom Restoration Act (RFRA), a law enacted to protect individuals from laws that substantially burden their exercise of religion. They are left, they assert, with a choice of providing objectionable coverage or paying a fine, a substantial burden on their freedom of religion.

The key issue before the Court is whether secular for-profit corporations can avoid complying with the legal mandates of the ACA based on the religious beliefs of their owners. To date, five federal circuit courts have ruled on the RFRA claim. Some have determined that corporations have no religious rights. Others have found the opposite. The Supreme Court will attempt to set the path for lower courts to follow.

The outcome of these cases will have a profound effect on women’s health, and may be felt much more broadly in our health-care system. If a business owner can opt out of one sort of coverage based on his or her religious beliefs, then wouldn’t that rule apply to other areas of health care? Employers might choose not to cover childhood immunizations, blood transfusions, or maternity care for single workers. Allowing employers to pick and choose can be risky business.

ACOG joins an amicus brief

ACOG partnered with a number of other preeminent health-care organizations, including the American Academy of Pediatrics, the American College of Nurse-Midwives, the American Society for Reproductive Medicine, the Society for Maternal-Fetal Medicine, Physicians for Reproductive Health, and the International Association of Forensic Nurses, to prepare an amicus brief to the Court on these cases.

The arguments we and our colleagues put forward centered on two points:

- Employers should not be allowed to interfere in the provider-patient relationship

- Allowing employers to veto coverage based on their own religious beliefs has broad and troubling public health implications.

Contraception is an essential component of women’s health care. The Supreme Court could unravel this important new guarantee or protect it for today’s and future generations.

Acknowledgment

The author thanks and acknowledges Sara Needleman Kline, JD, Deputy General Counsel, ACOG, for her helpful review and comments.

WE WANT TO HEAR FROM YOU!

Share your thoughts on this article or on any topic relevant to ObGyns and women’s health practitioners. Tell us which topics you’d like to see covered in future issues, and what challenges you face in daily practice. We will consider publishing your letter in a future issue. Send your letter to: obg@frontlinemedcom.com Please include the city and state in which you practice. Stay in touch! Your feedback is important to us!

- Kaiser Family Foundation. 2013 Employer Health Benefits Survey. http://kff.org/private-insurance/report/2013-employer-health-benefits/. Published August 20, 2013. Accessed March 27, 2014.

- Office of the US Federal Register. Definition of Grandfathered Health Plan Coverage in Paragraph (a) of 26 CFR 54.9815-1251T, 29 CFR 2590.715-1251, and 45 CFR 147.140 of These Interim Final Regulations. https://www.federalregister.gov/articles/2010/06/17/2010-14488/interim-final-rules-for-group-health-plans-and-health-insurance-coverage-relating-to-status-as-a#h-11. Published June 17, 2010. Accessed March 25, 2014.

- Kaiser Family Foundation. 2013 Employer Health Benefits Survey. http://kff.org/private-insurance/report/2013-employer-health-benefits/. Published August 20, 2013. Accessed March 27, 2014.

- Office of the US Federal Register. Definition of Grandfathered Health Plan Coverage in Paragraph (a) of 26 CFR 54.9815-1251T, 29 CFR 2590.715-1251, and 45 CFR 147.140 of These Interim Final Regulations. https://www.federalregister.gov/articles/2010/06/17/2010-14488/interim-final-rules-for-group-health-plans-and-health-insurance-coverage-relating-to-status-as-a#h-11. Published June 17, 2010. Accessed March 25, 2014.