User login

Characteristics of Applicants and Recipients of the Veterans Affairs Home Loan Program

The US Department of Veterans Affairs (VA) Home Loan Program, administered by the Veterans Benefits Administration (VBA), is a unique benefit for veterans, active-duty service members, National Guard and Reserve members, and eligible surviving spouses. Established in 1944, the program aims to help these individuals achieve homeownership by leveraging a third-party guarantee, typically from a government agency, to enhance access to credit and improve loan terms for borrowers who may not meet conventional loan qualifications.1 Since its inception, the VA has guaranteed > 28.5 million loans, enabling millions of veterans to buy, build, repair, retain, or adapt homes for personal occupancy.2 The program is designed to support veterans and eligible individuals to become homeowners, recognizing homeownership as a pathway to financial stability and community integration. VA home loans are provided by private lenders (eg, banks, mortgage companies) with a portion guaranteed by the VA, which reduces the risk for lenders and enables them to offer competitive terms, such as no down payment and lower interest rates, making homeownership more accessible to veterans.2

Eligibility criteria for the VA Home Loan Program include military service criteria such as active-duty service members with ≥ 90 continuous days of service; veterans with an honorable discharge meeting minimum service requirements; individuals who served in the National Guard/Reserve for ≥ 90 days of active service or 6 years of service with an honorable discharge; and surviving spouses of veterans who died in service or from a service-connected disability, were designated as missing in action/ prisoner of war, and the spouse is receiving Dependency and Indemnity Compensation. Financial criteria also apply: borrowers must meet lender requirements for credit and income (although VA loans are more flexible than conventional loans) and the home must be for personal occupancy rather than an investment property.3

A June 2025 PubMed literature search did not reveal any prior research on the VA Home Loan Program, although a limited number of studies tackled a wide range of issues related to federal and private home loans.4-12 To our knowledge, there is no prior published examination of the VA Home Loan Program. Understanding VA Home Loan Program usage among Veterans Health Administration (VHA) users can inform the future direction of the program. The VHA operates the largest integrated US health care system, serving > 9 million enrolled veterans annually at 1321 facilities, including 172 medical centers and 1138 outpatient clinics, providing primary and specialized health care, and related medical and social support services for enrolled veterans, including those who are experiencing housing instability or homelessness.13 Specialized VHA programs for homeless veterans include housing, employment, health care, justice, and re-entryrelated services in collaboration with federal and community partners.14 Housing instability has been defined as the state of being at risk of losing housing due to challenges such as difficulties paying rent, overcrowding, frequent relocation, and a substantial proportion of income spent on housing.15,16 Homelessness is a severe manifestation of housing instability that has been defined as the lack of stable, safe, and functioning housing.17,18

Health care and social services, including those that address housing instability and homelessness, are major priorities for the VHA and VBA.19 The VA Home Loan Program may represent an important resource to help veterans achieve long-term housing stability through home ownership. There has been wide public concern about housing affordability and the ability of many Americans, including veterans, to achieve home ownership.20 Homeownership is considered an important part of developing financial assets and achieving financial stability. Lowincome veterans, in particular, may benefit from this program as a national study found that 8.0% of low-income veterans and 13.9% of veterans with a history of homelessness have previously experienced a home foreclosure. 21 A greater understanding of who applies for and receives assistance from the VA Home Loan Program would inform homelessness prevention services and future planning for this program.

We conducted a quality improvement (QI) project on behalf of the VHA Homeless Programs Office and in partnership with the VBA. Our goals were to: (1) describe the annual number of applicants and recipients of the VA Home Loan Program by age group, sex, race/ethnicity, presence of any diagnosed substance use and/or mental health disorder, and history of homelessness; and (2) compare demographic, clinical, and homelessness characteristics among individuals who apply and are granted a loan through this program, individuals who apply and are denied a loan through this program, and individuals who do not apply for a loan through this program.

Methods

This project involved linked VA administrative national databases and was undertaken by the VHA Homeless Programs Office in partnership with the VBA. Specifically, VHA and VBA databases were linked together using veteran identifiers and all data were managed and analyzed on secure VA servers. The project followed VA’s Program Guide 1200.21 for nonresearch activities and institutional review board approval was waived through sponsorship by the VA Homeless Programs Office. The VHA Corporate Data Warehouse (CDW) was accessed to obtain data from the Homeless Operations Management and Evaluation System (HOMES) and other clinical data systems used by VHA clinicians and administrators that capture diagnoses, workload, and other health care data.22,23 HOMES collects intake, progress, and outcome data on homeless veterans within its care system that enables the VA to assess the effectiveness of programs and strategically allocate resources to prevent homelessness.24,25

A list of veterans who filed disability compensation and pension claims was obtained from the VBA Office of Performance Analysis and Integrity, including Social Security number, name, city and state, date of claim submission, grant or increase in benefits, homeless status, VA home loan approval, and homeless aid for dependent children from fiscal year (FY) 2022 through FY 2024. VBA data were linked to VHA CDW electronic health record data from veterans who sought VA health care services and HOMES data on veteran participation in homeless programs who were also experiencing homelessness. VHA data included demographic characteristics (eg, sex, age, race, marital status, combat service) at an index date (earliest visit to the VHA between October 1, 2021, and September 30, 2024); military sexual trauma; clinical characteristics within 12 months prior to the index date (VHA disability rating, substance use disorder [SUD] diagnosis, mental health disorder diagnosis, Charlson Comorbidity Index [CCI] score), and homelessness experience ≤ 5 years prior to the index date.

History of homelessness ≤ 5 years prior to the index date was determined using an operational definition of homelessness based on multiple indicators, including International Classification of Diseases, Tenth Revision, Clinical Modification (ICD-10-CM) diagnostic code Z59.0; clinic stop codes or HOMES records indicating VA homeless programs clinical encounters; or a positive screen on an annual homelessness screener.16 US Department of Housing and Urban Development-VA Supportive Housing enrollees were excluded because they are considered to no longer be experiencing homelessness, and Veterans Justice Program enrollees were excluded because the program primarily focuses on serving criminal justice-involved veterans. The CCI predicts the risk of death ≤ 1 year by assessing the number and severity of a patient’s coexisting health conditions and is a valuable tool for understanding a patient’s overall health burden, aiding in clinical decision-making and evaluation research studies.26-29 Diagnoses based on ICD-10-CM codes were used to determine SUDs, mental health disorders, and CCI score, using methods that have been described in other publications.30

Population

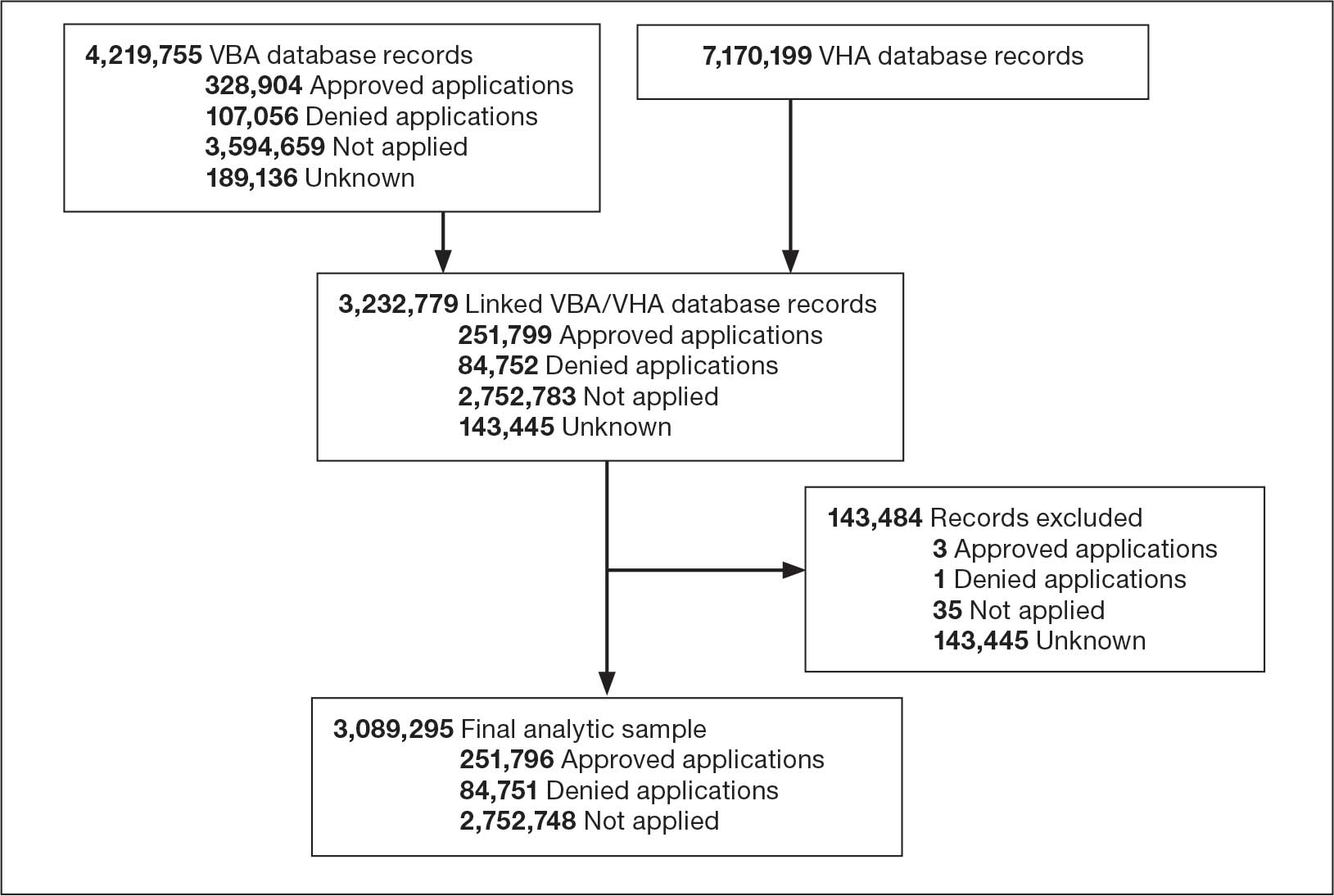

The VBA cohort of veterans requesting benefits was further restricted to those who met the following eligibility criteria: (1) requested VA benefits FYs 2022 to 2024; (2) sought VHA services ≥ 1 time between FY 2022 and 2024; (3) had matching VBA/VHA records; (4) had no missing data on claim status and/ or demographic, clinical, and homelessness characteristics; and (5) had known home loan status FYs 2022 to 2024. The original VBA dataset consisted of 4,219,755 records and the original VHA dataset consisted of 7,170,199 records (Figure 1). The final linked VBA/VHA dataset after excluding 29 records with missing data on sex, 7 with missing data on age, 6 with missing data on marital status, and an additional 143,444 with unknown VBA claim status, consisted of 3,089,295 records corresponding to 2,260,851 unique veterans. Specifically, 251,796 records corresponded to veterans who had applied and received a loan, 84,751 to veterans who had applied and were nonrecipients of a loan, and 2,752,748 to veterans who did not apply for a loan.

Abbreviations: FY, fiscal year; VBA, Veterans Benefits Administration; VHA, Veterans Health Administration.

Statistical Analysis

All statistical analyses were performed using SAS Enterprise Guide, an application that provides a point-and-click interface for data access, analysis, and management, accommodating both code-based and visual programming. 31 First, we relied on the final analytic sample to calculate the annual proportions of veterans who applied for and/or received a loan through the VA Home Loan Program. We also generated descriptive statistics stratified by age group, sex, race/ethnicity, SUD, mental health disorder, and homelessness, overall and within each FY. Pearson χ2 and Cochran-Armitage trend tests were applied to examine differences in application and receipt of a home loan by baseline characteristics and FY, respectively. Second, we conducted bivariate and multivariable analyses to compare demographic, clinical, and homelessness characteristics between 3 groups of veterans as they pertain to the VA Home Loan Program. Veterans who applied and were nonrecipients of a loan (group 1), veterans who applied and were recipients of a loan (group 2), and veterans who did not apply for a loan (group 3). Similar analyses compared VA Home Loan Program applicants who were recipients of a home loan vs VA Home Loan Program applicants who were nonrecipients of a home loan. Multinomial and binary logistic regression models were constructed to estimate the relative risk ratio (RR) and odds ratio (OR) with 95% CIs for comparisons between these distinct groups on demographic, clinical, and homelessness characteristics. Two-sided statistical tests were evaluated at α = 0.05.

Results

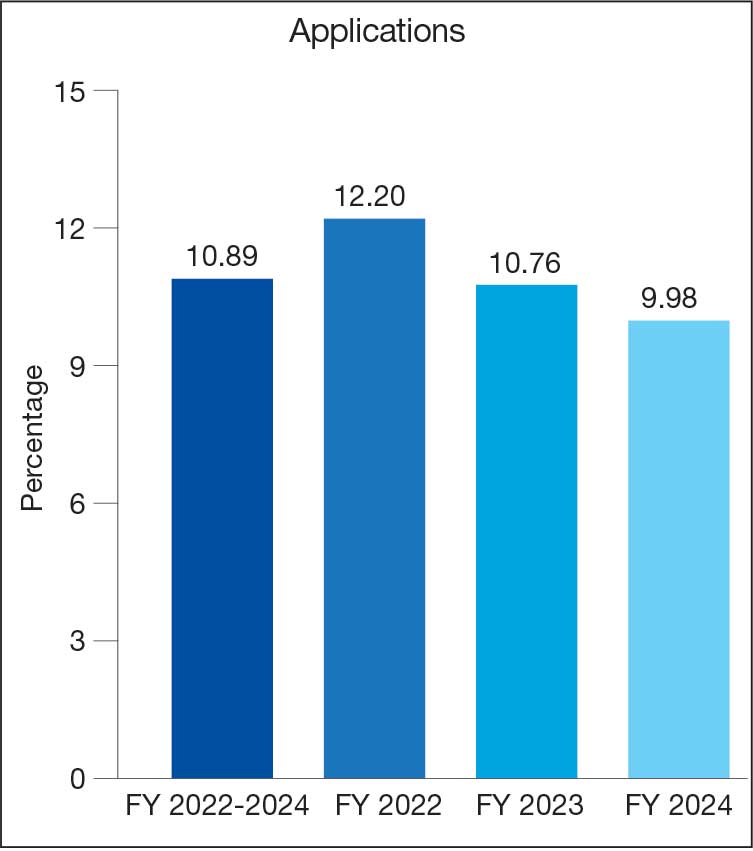

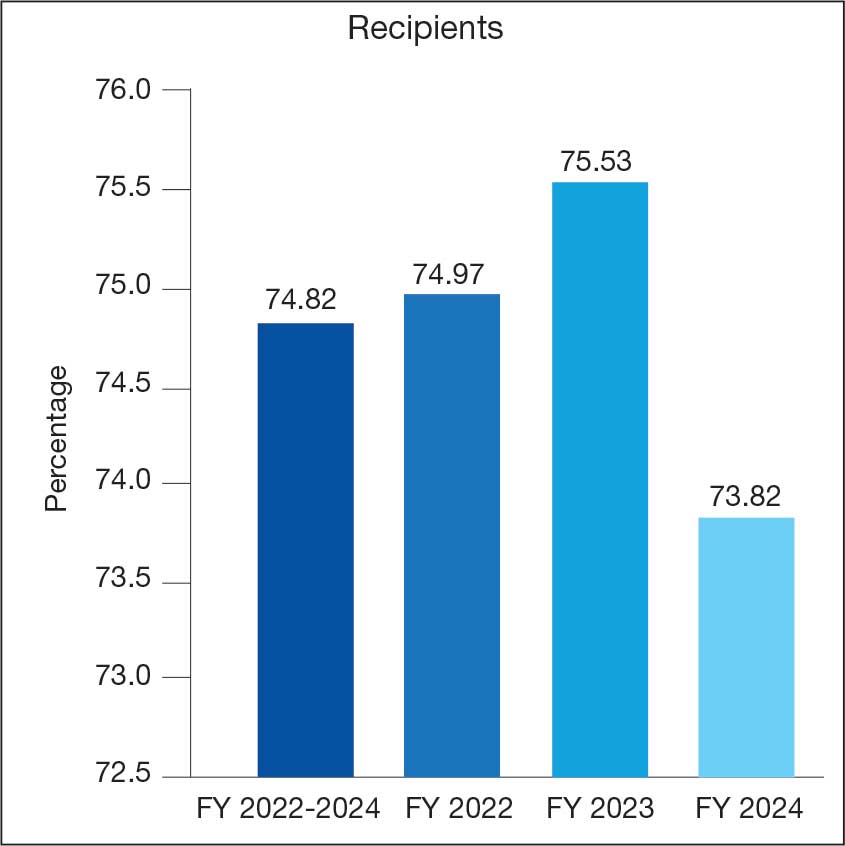

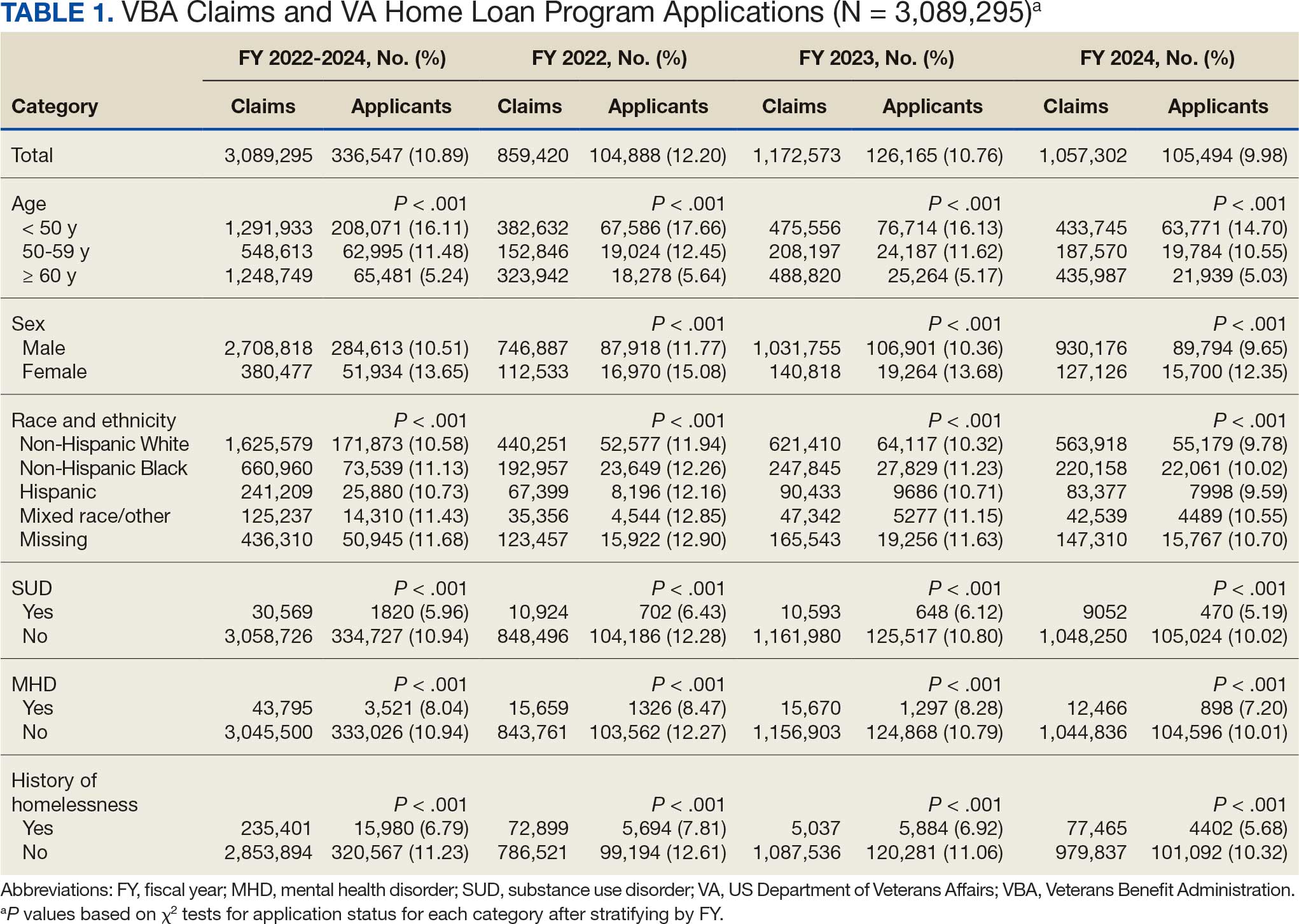

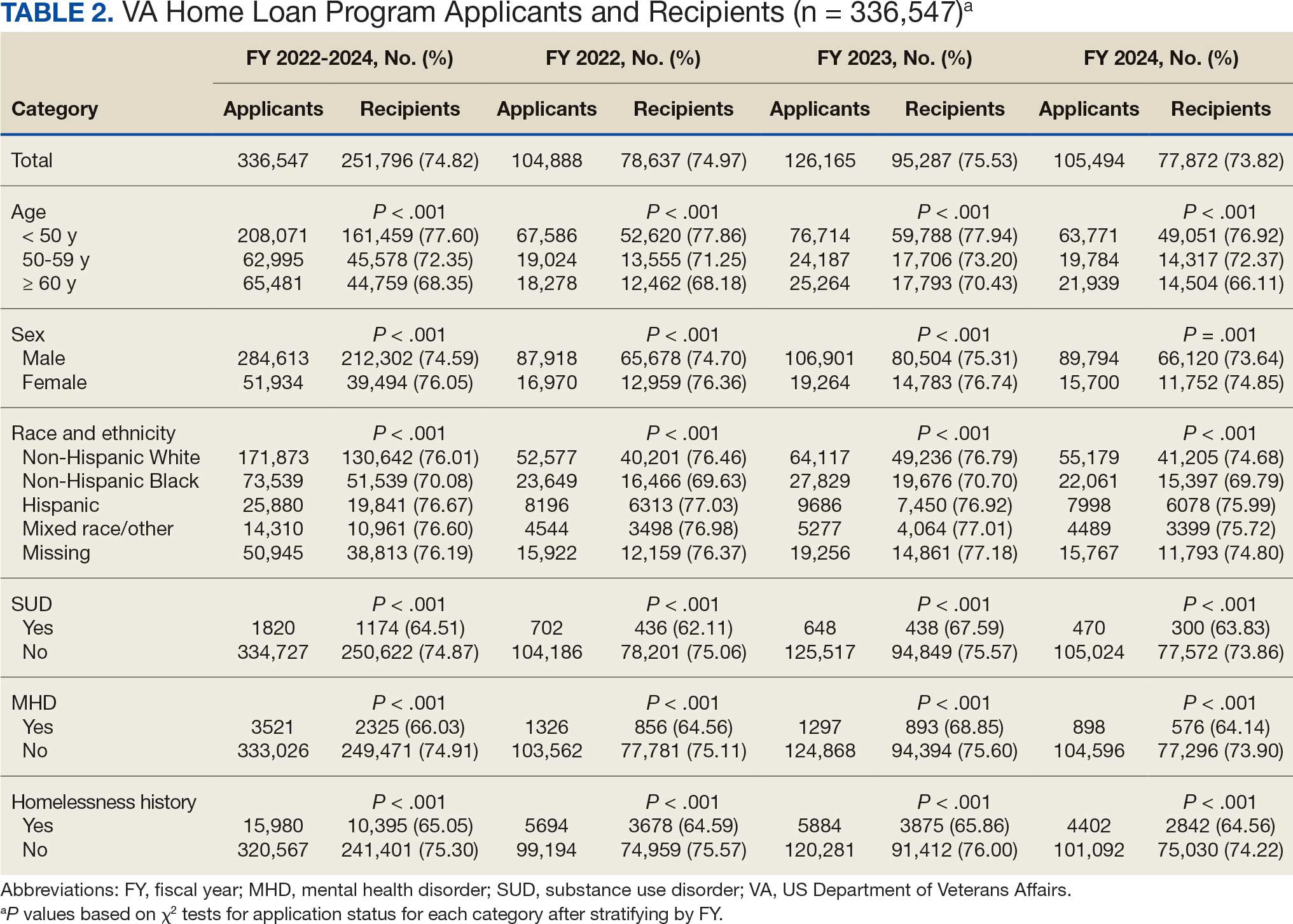

Tables 1 and 2 present the number of VBA applicants, including those who applied for and received benefits through the VA Home Loan Program, by age group, sex, race/ethnicity, as well as histories of SUDs, mental health disorders, and homelessness, overall, and by FY. As shown in Figure 2, 336,547 of 3,089,295 VBA applications (10.9%) pertained to the VA Home Loan Program, with a statistically significant decline in application rates, from 12.2% in FY 2022 to 9.9% in FY 2024 (P < .001 for trend). Among 336,547 veterans who applied for the VA Home Loan Program, 251,796 (74.8%) received a home loan during FYs 2022 to 2024, ranging between 73.8% for FY 2024 and 75.5% for FY 2023 (P < .001 for trend).

Veterans Affairs Home Loan Program, fiscal years (FY) 2022-2024.

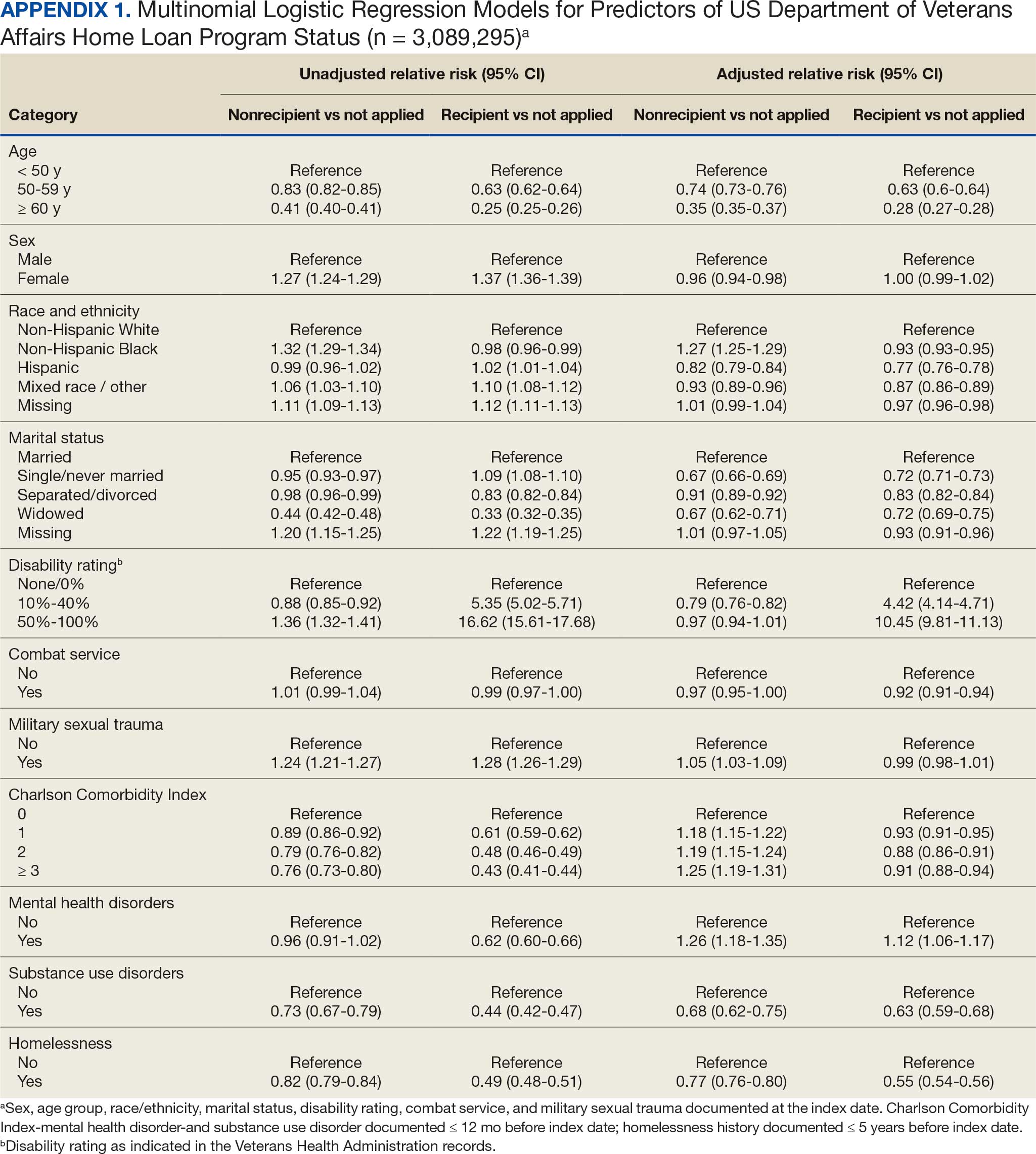

Multinomial logistic regression models for demographic, clinical, and homelessness characteristics as predictors of VA Home Loan Program status are provided in Appendix 1. Based on the fully adjusted model, compared with veterans who did not apply to the VA Home Loan Program, those who applied for a home loan were less likely to be aged ≥ 50 years, unmarried, Hispanic ethnicity, mixed race, or other race, diagnosed with a SUD, or history of homelessness. Veterans with higher VA service-connected disability ratings were more frequently recipients of VA home loans, whereas those who self-identified as non-Hispanic Black and those with higher CCI scores were less frequently recipients of VA home loans. Finally, those with mental health disorders were more likely than their counterparts to be applicants (recipients or nonrecipients) of VA home loans.

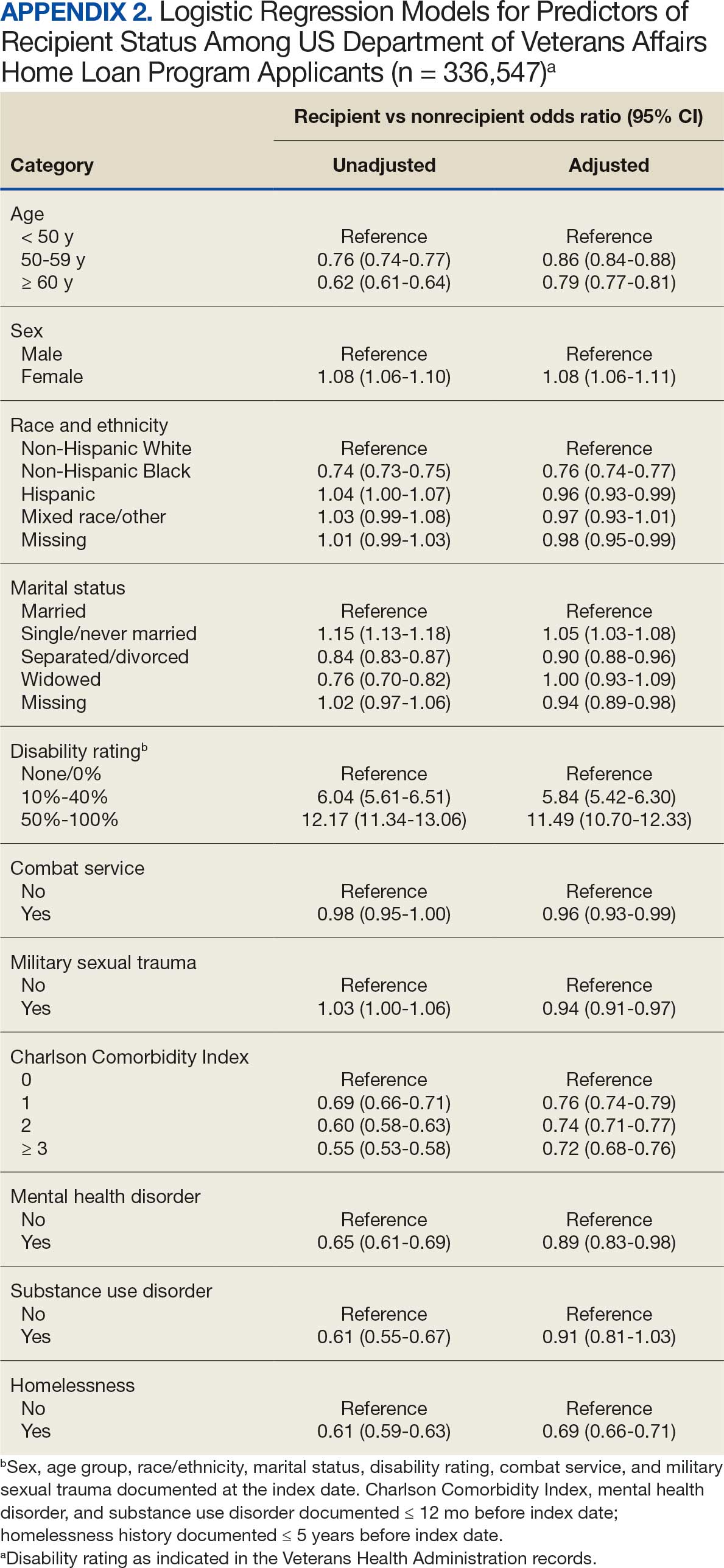

Binary logistic regression models for demographic, clinical, and homelessness characteristics as predictors of receipt status among applicants to the VA Home Loan Program are provided in Appendix 2. Among applicants, those who were granted a VA home loan were less likely to be aged ≥ 50 years; have a CCI score > 0; have experienced combat service and/or military sexual trauma; be diagnosed with a SUD and/or mental health disorder; or to have a history of homelessness compared with those denied a VA home loan. Applicants granted a VA home loan were also more likely to be female, non-Hispanic White, single or never married, and/or have a VA service-connected disability ratings > 0%.

Discussion

The VA Home Loan Program is a unique benefit and resource for eligible veterans that may be increasingly important in a time of growing concern about the affordability of housing for many Americans. Research on other federally-supported home loan programs as well as private home mortgage programs has been mostly conducted in the economic realm, and studies focused on understanding these programs from a health care system perspective have been sparse.32,33 However, there is a large body of literature documenting the importance of stable, safe, and secure housing on health and well-being.34-37 This study did not focus on evaluating the effects of the VA Home Loan Program, because we wanted to first examine the characteristics of veterans who benefited from the program and how they differed from veterans who did not apply or did apply but had a denied application.

Our findings suggest that several thousands of veterans benefit from the VA Home Loan Program each year. For historical context, the time period examined was one of economic downturn with rising costs of living, including housing, and steady increases in homelessness as reported in the annual point-in-time count of sheltered and unsheltered people experiencing homelessness on a single night as mandated by the US Department of Housing and Urban Development.38-40 The Sergeant First Class Heath Robinson Honoring Our Promise to Address Comprehensive Toxics (PACT) Act of 2022 expanded health care and benefits for veterans exposed to burn pits, Agent Orange, and other toxic substances, resulting in more VA disability benefit claims, including large retroactive payments.41-43 Anecdotally, the VBA has noted that the PACT Act helped some homeless veterans with funds and stability to exit homelessness and enroll in the VA Home Loan Program.

Our analysis suggests that beneficiaries of the VA Home Loan Program were frequently aged < 50 years, female, of non-Hispanic White race, and did not have histories of psychiatric disorders or homelessness. Most of these demographic and clinical characteristics were not surprising given the composition of the veteran population, although in-depth analyses are needed to examine sex differences that may have led to more females than males benefiting from the VA Home Loan Program. In addition, it was notable that many younger and non-Hispanic Black veterans had applied. While relatively few veterans with SUDs benefited from the VA Home Loan Program, few had applied. Research is warranted into why veterans with SUDs are less likely to apply for home loans. Quite surprisingly, a sizable proportion of veterans with histories of homelessness reported they had applied to the VA Home Loan Program, although they were less likely than veterans who had not experienced homelessness to be granted a loan.

The examination of differences between veterans who did not apply, were granted, and denied a loan through the VA Home Loan Program revealed several key predictors of application outcomes in multivariable models. Specifically, veterans who applied for home loans were less likely to be aged ≥ 50 years, unmarried, of Hispanic, mixed, or other race/ethnicity, diagnosed with an SUD, or have a history of homelessness. Veterans with higher disability ratings were less frequently denied and more frequently approved, while non-Hispanic Black veterans and those with higher CCI scores were more frequently denied and less frequently approved. VBA applicants with mental health disorders were also more likely to apply for a home loan. Conversely, those granted a home loan were more likely than those denied a home loan to be female, non-Hispanic White, single/unmarried, or to have > 0% VA service-connected disability rating, but less likely to be aged ≥ 50 years, have CCI score > 0, be diagnosed with psychiatric disorders, or have a history of homelessness.

Limitations

This analysis was restricted to a subset of FY 2022 to FY 2024 linked VBA/VHA databases (ie, to veterans who had both VBA and VHA records and met prespecified eligibility criteria). Despite the large number of linked records, a small percentage of these records corresponded to veterans who were applicants or recipients of the VA Home Loan Program. Future studies should expand the time frame to examine variations in application outcomes over time and by background characteristics of veterans enrolled in VHA care who applied for VBA benefits. In addition, we relied on data and ICD-10-CM diagnostic codes from existing electronic health records and claims data to define histories of homelessness, comorbidities, SUDs, and mental health disorders. Given the time-varying nature of these conditions, the temporal sequence of events was difficult to ascertain. Third, it is worth noting that these findings can only be generalized to veterans who applied for VBA benefits and met eligibility criteria, and that these veterans may differ in terms of their demographic and clinical characteristics from those who did not apply for these benefits.

Conclusions

This study analyzed data from 251,796 individuals who applied for and received a VA home loan, 84,751 who were denied a VA home loan, and 2,752,748 veterans who did not apply for a VA home loan from FY 2022 to FY 2024. Accordingly, 11% of applications pertained to the VA Home Loan Program, and 75% of VA Home Loan Program applicants received a home loan. Distinct demographic and clinical characteristics were observed for applicants and recipients of the VA Home Loan Program, which can set the stage for future planning and evaluation of the program. Despite the broad accessibility of veterans to the VA Home Loan Program, there were differences in approval rates among applicants based on sociodemographic and clinical characteristics. Further evaluation, perhaps using qualitative methods, is needed to better understand opportunities and challenges to achieving a VA home loan, especially among underserved veteran populations. Investigation and research can guide future recommendations for any development or corrective actions that can help increase access to veterans who can benefit from the program. Future analyses are also needed to compare veterans enrolled and not enrolled in the VA Home Loan Program on health care-related outcomes.

- US Department of Veterans Affairs. Home loans. Accessed April 1, 2026. https://www.benefits.va.gov/homeloans/

- Veterans United Home Loans. VA loans: the complete guide. Accessed April 1, 2026. https://www.veteransunited.com/va-loans/

- US Department of Veterans Affairs. VA-backed veterans home loans. Accessed April 1, 2026. https://www.va.gov/housing-assistance/home-loans/

- Choplin JM, Stark DP. Whispering sweet nothings: a review of verbal behaviors that undermine the effectiveness of government-mandated home-loan disclosures. Cogn Res Princ Implic. 2019;4:6. doi:10.1186/s41235-019-0154-7

- Evans M. Borrowing boon. More explore federal home loan banks backing. Mod Healthc. 2009;39:14.

- Hogarth M. A home loan: how—and how much? Nurs Times. 1973;69:908-909.

- Jacoby SF. Home Owners’ Loan Corporation maps and place-based injury risks: a complex history. Am J Public Health. 2023;113:356-358. doi:10.2105/AJPH.2023.307242

- Merrell C. Finance. Home: a loan. Nurs Times. 1996;92:61-64.

- Namin S, Xu W, Zhou Y, et al. The legacy of the Home Owners’ Loan Corporation and the political ecology of urban trees and air pollution in the United States. Soc Sci Med. 2020;246:112758. doi:10.1016/j.socscimed.2019.112758

- Namin S, Zhou Y, Xu W, et al. Persistence of mortgage lending bias in the United States: 80 years after the Home Owners’ Loan Corporation security maps. J Race Ethn City. 2022;3:70-94. doi:10.1080/26884674.2021.2019568

- Slottow R. The home loan program. J Natl Assoc Hosp Dev. 1990:43-45.

- Wang M, Chen H, Wang L. Locus of control and home mortgage loan behaviour. Int J Psychol. 2008;43:125-129. doi:10.1080/00207590801888760

- US Dept of Veterans Affairs. Veterans Health Administration. About VHA. Updated January 20, 2025. Accessed April 1, 2026. https://www.va.gov/health/aboutvha.asp

- US Dept of Veterans Affairs. VA homeless programs. Updated May 7, 2026. Accessed May 8, 2026. https://department.va.gov/homeless/

- DiTosto JD, Holder K, Soyemi E, et al. Housing instability and adverse perinatal outcomes: a systematic review. Am J Obstet Gynecol MFM. 2021;3:100477. doi:10.1016/j.ajogmf.2021.100477

- Tsai J, Szymkowiak D, Jutkowitz E. Developing an operational definition of housing instability and homelessness in Veterans Health Administration medical records. PLoS One. 2022;17:e0279973. doi:10.1371/journal.pone.0279973

- Fowler PJ, Hovmand PS, Marcal KE, et al. Solving homelessness from a complex systems perspective: insights for prevention responses. Annu Rev Public Health. 2019;40: 465-486. doi:10.1146/annurev-publhealth-040617-013553

- US Department of Health and Human Services. Healthy People 2030: housing instability. Accessed April 1, 2026. https://health.gov/healthypeople/priority-areas/social-determinants-health/literature-summaries/housing-instability

- US Department of Veterans Affairs. VA health care priorities. Accessed April 1, 2026. https://www.va.gov/health/priorities/index.asp

- Tsai J. Federal priorities to address homelessness as a community health problem. Fam Community Health. 2025;48:57-69.

- Tsai J, Hooshyar D. Prevalence of eviction, home foreclosure, and homelessness among low-income US veterans: the National Veteran Homeless and Other Poverty Experiences study. Public Health. 2022;213:181-188. doi:10.1016/j.puhe.2022.10.017

- US Department of Veterans Affairs. Corporate Data Warehouse (CDW). Accessed April 1, 2026. https://www.hsrd.research.va.gov/for_researchers/cdw.cfm

- Price LE, Shea K, Gephart S. The Veterans Affairs Corporate Data Warehouse: uses and implications for nursing research and practice. Nurs Adm Q. 2015;39:311-318. doi:10.1097/NAQ.0000000000000118

- US Department of Veterans Affairs. Homeless Operations Management and Evaluation System (HOMES) User Manual—Phase 1. April 19, 2011. Accessed April 1, 2026. https://www.adldata.org/wp-content/uploads/2016/07/homes.pdf

- Tsai J, Kasprow WJ, Rosenheck RA. Latent homeless risk profiles of a national sample of homeless veterans and their relation to program referral and admission patterns. Am J Public Health. 2013;103:S239-S247. doi:10.2105/AJPH.2013.301322

- Sundararajan V, Henderson T, Perry C, et al. New ICD-10 version of the Charlson comorbidity index predicted inhospital mortality. J Clin Epidemiol. 2004;57:1288-1294. doi:10.1016/j.jclinepi.2004.03.012

- Beydoun HA, Szymkowiak D, Beydoun MA, et al. Comparing major comorbidity indices as predictors of all-cause mortality in the Veterans Affairs health care system. J Clin Epidemiol. 2025;182:111778. doi:10.1016/j.jclinepi.2025.111778

- Charlson ME, Carrozzino D, Guidi J, et al. Charlson Comorbidity Index: a critical review of clinimetric properties. Psychother Psychosom. 2022;91:8-35. doi:10.1159/000521288

- Glasheen WP, Cordier T, Gumpina R, et al. Charlson Comorbidity Index: ICD-9 update and ICD-10 translation. Am Health Drug Benefits. 2019;12:188-197.

- Beydoun HA, Szymkowiak D, Kinney R, et al. Is the risk of Alzheimer’s disease and related dementias among US veterans influenced by the intersectionality of housing status, HIV/AIDS, hepatitis C, and psychiatric disorders? J Gerontol A Biol Sci Med Sci. 2024;79:glae153. doi:10.1093/gerona/glae153

- SAS Institute. SAS Enterprise Guide. Accessed April 1, 2026. https://www.sas.com/en_us/software/enterprise-guide/features-list.html

- Agarwal S, Amromin G, Chomsisengphet S, et al. Mortgage refinancing, consumer spending, and competition: evidence from the Home Affordable Refinance Program. Rev Econ Stud. 2023;90:499-537.

- Ashcraft A, Bech ML, Frame WS. The Federal Home Loan Bank System: the lender of next-to-last resort? J Money Credit Bank. 2010;42:551-583.

- Gibson M, Petticrew M, Bambra C, et al. Housing and health inequalities: a synthesis of systematic reviews of interventions aimed at different pathways linking housing and health. Health Place. 2011;17:175-184. doi:10.1016/j.healthplace.2010.09.011

- Shaw M. Housing and public health. Annu Rev Public Health. 2004; 25:397-418. doi:10.1146/annurev.publhealth.25.101802.123036

- Thomson H, Petticrew M, Morrison D. Health effects of housing improvement: systematic review of intervention studies. BMJ. 2001;323:187-190. doi:10.1136/bmj.323.7306.187

- Tsai J. Theorizing pathways between eviction filings and increased mortality risk. JAMA. 2024;331:570-571. doi:10.1001/jama.2023.27978

- Bernanke B, Blanchard O. What caused the US pandemicera inflation? Am Econ J Macroecon. 2025;17:1-35.

- Hall SG, Tavlas GS, Wang Y. Drivers and spillover effects of inflation: the United States, the euro area, and the United Kingdom. J Int Money Finance. 2023;131:1-13.

- US Department of Housing and Urban Development. Point-in-Time Count and Housing Inventory Count. Accessed April 1, 2026. https://www.hudexchange.info/programs/hdx/pit-hic/

- Beckman AL, Jacobs J, Elnahal SM. The PACT Act: expanding coverage and access for veterans. JAMA. 2024;332:1423-1424. doi:10.1001/jama.2024.16013

- Zychowicz ME. The PACT Act: enhancing health care access for military personnel and veterans. N C Med J. 2023;84:379-380. doi:10.18043/001c.89208

- US Department of Veterans Affairs. The PACT Act and your VA benefits. April 2, 2026. https://www.va.gov/resources/the-pact-act-and-your-va-benefits/

The US Department of Veterans Affairs (VA) Home Loan Program, administered by the Veterans Benefits Administration (VBA), is a unique benefit for veterans, active-duty service members, National Guard and Reserve members, and eligible surviving spouses. Established in 1944, the program aims to help these individuals achieve homeownership by leveraging a third-party guarantee, typically from a government agency, to enhance access to credit and improve loan terms for borrowers who may not meet conventional loan qualifications.1 Since its inception, the VA has guaranteed > 28.5 million loans, enabling millions of veterans to buy, build, repair, retain, or adapt homes for personal occupancy.2 The program is designed to support veterans and eligible individuals to become homeowners, recognizing homeownership as a pathway to financial stability and community integration. VA home loans are provided by private lenders (eg, banks, mortgage companies) with a portion guaranteed by the VA, which reduces the risk for lenders and enables them to offer competitive terms, such as no down payment and lower interest rates, making homeownership more accessible to veterans.2

Eligibility criteria for the VA Home Loan Program include military service criteria such as active-duty service members with ≥ 90 continuous days of service; veterans with an honorable discharge meeting minimum service requirements; individuals who served in the National Guard/Reserve for ≥ 90 days of active service or 6 years of service with an honorable discharge; and surviving spouses of veterans who died in service or from a service-connected disability, were designated as missing in action/ prisoner of war, and the spouse is receiving Dependency and Indemnity Compensation. Financial criteria also apply: borrowers must meet lender requirements for credit and income (although VA loans are more flexible than conventional loans) and the home must be for personal occupancy rather than an investment property.3

A June 2025 PubMed literature search did not reveal any prior research on the VA Home Loan Program, although a limited number of studies tackled a wide range of issues related to federal and private home loans.4-12 To our knowledge, there is no prior published examination of the VA Home Loan Program. Understanding VA Home Loan Program usage among Veterans Health Administration (VHA) users can inform the future direction of the program. The VHA operates the largest integrated US health care system, serving > 9 million enrolled veterans annually at 1321 facilities, including 172 medical centers and 1138 outpatient clinics, providing primary and specialized health care, and related medical and social support services for enrolled veterans, including those who are experiencing housing instability or homelessness.13 Specialized VHA programs for homeless veterans include housing, employment, health care, justice, and re-entryrelated services in collaboration with federal and community partners.14 Housing instability has been defined as the state of being at risk of losing housing due to challenges such as difficulties paying rent, overcrowding, frequent relocation, and a substantial proportion of income spent on housing.15,16 Homelessness is a severe manifestation of housing instability that has been defined as the lack of stable, safe, and functioning housing.17,18

Health care and social services, including those that address housing instability and homelessness, are major priorities for the VHA and VBA.19 The VA Home Loan Program may represent an important resource to help veterans achieve long-term housing stability through home ownership. There has been wide public concern about housing affordability and the ability of many Americans, including veterans, to achieve home ownership.20 Homeownership is considered an important part of developing financial assets and achieving financial stability. Lowincome veterans, in particular, may benefit from this program as a national study found that 8.0% of low-income veterans and 13.9% of veterans with a history of homelessness have previously experienced a home foreclosure. 21 A greater understanding of who applies for and receives assistance from the VA Home Loan Program would inform homelessness prevention services and future planning for this program.

We conducted a quality improvement (QI) project on behalf of the VHA Homeless Programs Office and in partnership with the VBA. Our goals were to: (1) describe the annual number of applicants and recipients of the VA Home Loan Program by age group, sex, race/ethnicity, presence of any diagnosed substance use and/or mental health disorder, and history of homelessness; and (2) compare demographic, clinical, and homelessness characteristics among individuals who apply and are granted a loan through this program, individuals who apply and are denied a loan through this program, and individuals who do not apply for a loan through this program.

Methods

This project involved linked VA administrative national databases and was undertaken by the VHA Homeless Programs Office in partnership with the VBA. Specifically, VHA and VBA databases were linked together using veteran identifiers and all data were managed and analyzed on secure VA servers. The project followed VA’s Program Guide 1200.21 for nonresearch activities and institutional review board approval was waived through sponsorship by the VA Homeless Programs Office. The VHA Corporate Data Warehouse (CDW) was accessed to obtain data from the Homeless Operations Management and Evaluation System (HOMES) and other clinical data systems used by VHA clinicians and administrators that capture diagnoses, workload, and other health care data.22,23 HOMES collects intake, progress, and outcome data on homeless veterans within its care system that enables the VA to assess the effectiveness of programs and strategically allocate resources to prevent homelessness.24,25

A list of veterans who filed disability compensation and pension claims was obtained from the VBA Office of Performance Analysis and Integrity, including Social Security number, name, city and state, date of claim submission, grant or increase in benefits, homeless status, VA home loan approval, and homeless aid for dependent children from fiscal year (FY) 2022 through FY 2024. VBA data were linked to VHA CDW electronic health record data from veterans who sought VA health care services and HOMES data on veteran participation in homeless programs who were also experiencing homelessness. VHA data included demographic characteristics (eg, sex, age, race, marital status, combat service) at an index date (earliest visit to the VHA between October 1, 2021, and September 30, 2024); military sexual trauma; clinical characteristics within 12 months prior to the index date (VHA disability rating, substance use disorder [SUD] diagnosis, mental health disorder diagnosis, Charlson Comorbidity Index [CCI] score), and homelessness experience ≤ 5 years prior to the index date.

History of homelessness ≤ 5 years prior to the index date was determined using an operational definition of homelessness based on multiple indicators, including International Classification of Diseases, Tenth Revision, Clinical Modification (ICD-10-CM) diagnostic code Z59.0; clinic stop codes or HOMES records indicating VA homeless programs clinical encounters; or a positive screen on an annual homelessness screener.16 US Department of Housing and Urban Development-VA Supportive Housing enrollees were excluded because they are considered to no longer be experiencing homelessness, and Veterans Justice Program enrollees were excluded because the program primarily focuses on serving criminal justice-involved veterans. The CCI predicts the risk of death ≤ 1 year by assessing the number and severity of a patient’s coexisting health conditions and is a valuable tool for understanding a patient’s overall health burden, aiding in clinical decision-making and evaluation research studies.26-29 Diagnoses based on ICD-10-CM codes were used to determine SUDs, mental health disorders, and CCI score, using methods that have been described in other publications.30

Population

The VBA cohort of veterans requesting benefits was further restricted to those who met the following eligibility criteria: (1) requested VA benefits FYs 2022 to 2024; (2) sought VHA services ≥ 1 time between FY 2022 and 2024; (3) had matching VBA/VHA records; (4) had no missing data on claim status and/ or demographic, clinical, and homelessness characteristics; and (5) had known home loan status FYs 2022 to 2024. The original VBA dataset consisted of 4,219,755 records and the original VHA dataset consisted of 7,170,199 records (Figure 1). The final linked VBA/VHA dataset after excluding 29 records with missing data on sex, 7 with missing data on age, 6 with missing data on marital status, and an additional 143,444 with unknown VBA claim status, consisted of 3,089,295 records corresponding to 2,260,851 unique veterans. Specifically, 251,796 records corresponded to veterans who had applied and received a loan, 84,751 to veterans who had applied and were nonrecipients of a loan, and 2,752,748 to veterans who did not apply for a loan.

Abbreviations: FY, fiscal year; VBA, Veterans Benefits Administration; VHA, Veterans Health Administration.

Statistical Analysis

All statistical analyses were performed using SAS Enterprise Guide, an application that provides a point-and-click interface for data access, analysis, and management, accommodating both code-based and visual programming. 31 First, we relied on the final analytic sample to calculate the annual proportions of veterans who applied for and/or received a loan through the VA Home Loan Program. We also generated descriptive statistics stratified by age group, sex, race/ethnicity, SUD, mental health disorder, and homelessness, overall and within each FY. Pearson χ2 and Cochran-Armitage trend tests were applied to examine differences in application and receipt of a home loan by baseline characteristics and FY, respectively. Second, we conducted bivariate and multivariable analyses to compare demographic, clinical, and homelessness characteristics between 3 groups of veterans as they pertain to the VA Home Loan Program. Veterans who applied and were nonrecipients of a loan (group 1), veterans who applied and were recipients of a loan (group 2), and veterans who did not apply for a loan (group 3). Similar analyses compared VA Home Loan Program applicants who were recipients of a home loan vs VA Home Loan Program applicants who were nonrecipients of a home loan. Multinomial and binary logistic regression models were constructed to estimate the relative risk ratio (RR) and odds ratio (OR) with 95% CIs for comparisons between these distinct groups on demographic, clinical, and homelessness characteristics. Two-sided statistical tests were evaluated at α = 0.05.

Results

Tables 1 and 2 present the number of VBA applicants, including those who applied for and received benefits through the VA Home Loan Program, by age group, sex, race/ethnicity, as well as histories of SUDs, mental health disorders, and homelessness, overall, and by FY. As shown in Figure 2, 336,547 of 3,089,295 VBA applications (10.9%) pertained to the VA Home Loan Program, with a statistically significant decline in application rates, from 12.2% in FY 2022 to 9.9% in FY 2024 (P < .001 for trend). Among 336,547 veterans who applied for the VA Home Loan Program, 251,796 (74.8%) received a home loan during FYs 2022 to 2024, ranging between 73.8% for FY 2024 and 75.5% for FY 2023 (P < .001 for trend).

Veterans Affairs Home Loan Program, fiscal years (FY) 2022-2024.

Multinomial logistic regression models for demographic, clinical, and homelessness characteristics as predictors of VA Home Loan Program status are provided in Appendix 1. Based on the fully adjusted model, compared with veterans who did not apply to the VA Home Loan Program, those who applied for a home loan were less likely to be aged ≥ 50 years, unmarried, Hispanic ethnicity, mixed race, or other race, diagnosed with a SUD, or history of homelessness. Veterans with higher VA service-connected disability ratings were more frequently recipients of VA home loans, whereas those who self-identified as non-Hispanic Black and those with higher CCI scores were less frequently recipients of VA home loans. Finally, those with mental health disorders were more likely than their counterparts to be applicants (recipients or nonrecipients) of VA home loans.

Binary logistic regression models for demographic, clinical, and homelessness characteristics as predictors of receipt status among applicants to the VA Home Loan Program are provided in Appendix 2. Among applicants, those who were granted a VA home loan were less likely to be aged ≥ 50 years; have a CCI score > 0; have experienced combat service and/or military sexual trauma; be diagnosed with a SUD and/or mental health disorder; or to have a history of homelessness compared with those denied a VA home loan. Applicants granted a VA home loan were also more likely to be female, non-Hispanic White, single or never married, and/or have a VA service-connected disability ratings > 0%.

Discussion

The VA Home Loan Program is a unique benefit and resource for eligible veterans that may be increasingly important in a time of growing concern about the affordability of housing for many Americans. Research on other federally-supported home loan programs as well as private home mortgage programs has been mostly conducted in the economic realm, and studies focused on understanding these programs from a health care system perspective have been sparse.32,33 However, there is a large body of literature documenting the importance of stable, safe, and secure housing on health and well-being.34-37 This study did not focus on evaluating the effects of the VA Home Loan Program, because we wanted to first examine the characteristics of veterans who benefited from the program and how they differed from veterans who did not apply or did apply but had a denied application.

Our findings suggest that several thousands of veterans benefit from the VA Home Loan Program each year. For historical context, the time period examined was one of economic downturn with rising costs of living, including housing, and steady increases in homelessness as reported in the annual point-in-time count of sheltered and unsheltered people experiencing homelessness on a single night as mandated by the US Department of Housing and Urban Development.38-40 The Sergeant First Class Heath Robinson Honoring Our Promise to Address Comprehensive Toxics (PACT) Act of 2022 expanded health care and benefits for veterans exposed to burn pits, Agent Orange, and other toxic substances, resulting in more VA disability benefit claims, including large retroactive payments.41-43 Anecdotally, the VBA has noted that the PACT Act helped some homeless veterans with funds and stability to exit homelessness and enroll in the VA Home Loan Program.

Our analysis suggests that beneficiaries of the VA Home Loan Program were frequently aged < 50 years, female, of non-Hispanic White race, and did not have histories of psychiatric disorders or homelessness. Most of these demographic and clinical characteristics were not surprising given the composition of the veteran population, although in-depth analyses are needed to examine sex differences that may have led to more females than males benefiting from the VA Home Loan Program. In addition, it was notable that many younger and non-Hispanic Black veterans had applied. While relatively few veterans with SUDs benefited from the VA Home Loan Program, few had applied. Research is warranted into why veterans with SUDs are less likely to apply for home loans. Quite surprisingly, a sizable proportion of veterans with histories of homelessness reported they had applied to the VA Home Loan Program, although they were less likely than veterans who had not experienced homelessness to be granted a loan.

The examination of differences between veterans who did not apply, were granted, and denied a loan through the VA Home Loan Program revealed several key predictors of application outcomes in multivariable models. Specifically, veterans who applied for home loans were less likely to be aged ≥ 50 years, unmarried, of Hispanic, mixed, or other race/ethnicity, diagnosed with an SUD, or have a history of homelessness. Veterans with higher disability ratings were less frequently denied and more frequently approved, while non-Hispanic Black veterans and those with higher CCI scores were more frequently denied and less frequently approved. VBA applicants with mental health disorders were also more likely to apply for a home loan. Conversely, those granted a home loan were more likely than those denied a home loan to be female, non-Hispanic White, single/unmarried, or to have > 0% VA service-connected disability rating, but less likely to be aged ≥ 50 years, have CCI score > 0, be diagnosed with psychiatric disorders, or have a history of homelessness.

Limitations

This analysis was restricted to a subset of FY 2022 to FY 2024 linked VBA/VHA databases (ie, to veterans who had both VBA and VHA records and met prespecified eligibility criteria). Despite the large number of linked records, a small percentage of these records corresponded to veterans who were applicants or recipients of the VA Home Loan Program. Future studies should expand the time frame to examine variations in application outcomes over time and by background characteristics of veterans enrolled in VHA care who applied for VBA benefits. In addition, we relied on data and ICD-10-CM diagnostic codes from existing electronic health records and claims data to define histories of homelessness, comorbidities, SUDs, and mental health disorders. Given the time-varying nature of these conditions, the temporal sequence of events was difficult to ascertain. Third, it is worth noting that these findings can only be generalized to veterans who applied for VBA benefits and met eligibility criteria, and that these veterans may differ in terms of their demographic and clinical characteristics from those who did not apply for these benefits.

Conclusions

This study analyzed data from 251,796 individuals who applied for and received a VA home loan, 84,751 who were denied a VA home loan, and 2,752,748 veterans who did not apply for a VA home loan from FY 2022 to FY 2024. Accordingly, 11% of applications pertained to the VA Home Loan Program, and 75% of VA Home Loan Program applicants received a home loan. Distinct demographic and clinical characteristics were observed for applicants and recipients of the VA Home Loan Program, which can set the stage for future planning and evaluation of the program. Despite the broad accessibility of veterans to the VA Home Loan Program, there were differences in approval rates among applicants based on sociodemographic and clinical characteristics. Further evaluation, perhaps using qualitative methods, is needed to better understand opportunities and challenges to achieving a VA home loan, especially among underserved veteran populations. Investigation and research can guide future recommendations for any development or corrective actions that can help increase access to veterans who can benefit from the program. Future analyses are also needed to compare veterans enrolled and not enrolled in the VA Home Loan Program on health care-related outcomes.

The US Department of Veterans Affairs (VA) Home Loan Program, administered by the Veterans Benefits Administration (VBA), is a unique benefit for veterans, active-duty service members, National Guard and Reserve members, and eligible surviving spouses. Established in 1944, the program aims to help these individuals achieve homeownership by leveraging a third-party guarantee, typically from a government agency, to enhance access to credit and improve loan terms for borrowers who may not meet conventional loan qualifications.1 Since its inception, the VA has guaranteed > 28.5 million loans, enabling millions of veterans to buy, build, repair, retain, or adapt homes for personal occupancy.2 The program is designed to support veterans and eligible individuals to become homeowners, recognizing homeownership as a pathway to financial stability and community integration. VA home loans are provided by private lenders (eg, banks, mortgage companies) with a portion guaranteed by the VA, which reduces the risk for lenders and enables them to offer competitive terms, such as no down payment and lower interest rates, making homeownership more accessible to veterans.2

Eligibility criteria for the VA Home Loan Program include military service criteria such as active-duty service members with ≥ 90 continuous days of service; veterans with an honorable discharge meeting minimum service requirements; individuals who served in the National Guard/Reserve for ≥ 90 days of active service or 6 years of service with an honorable discharge; and surviving spouses of veterans who died in service or from a service-connected disability, were designated as missing in action/ prisoner of war, and the spouse is receiving Dependency and Indemnity Compensation. Financial criteria also apply: borrowers must meet lender requirements for credit and income (although VA loans are more flexible than conventional loans) and the home must be for personal occupancy rather than an investment property.3

A June 2025 PubMed literature search did not reveal any prior research on the VA Home Loan Program, although a limited number of studies tackled a wide range of issues related to federal and private home loans.4-12 To our knowledge, there is no prior published examination of the VA Home Loan Program. Understanding VA Home Loan Program usage among Veterans Health Administration (VHA) users can inform the future direction of the program. The VHA operates the largest integrated US health care system, serving > 9 million enrolled veterans annually at 1321 facilities, including 172 medical centers and 1138 outpatient clinics, providing primary and specialized health care, and related medical and social support services for enrolled veterans, including those who are experiencing housing instability or homelessness.13 Specialized VHA programs for homeless veterans include housing, employment, health care, justice, and re-entryrelated services in collaboration with federal and community partners.14 Housing instability has been defined as the state of being at risk of losing housing due to challenges such as difficulties paying rent, overcrowding, frequent relocation, and a substantial proportion of income spent on housing.15,16 Homelessness is a severe manifestation of housing instability that has been defined as the lack of stable, safe, and functioning housing.17,18

Health care and social services, including those that address housing instability and homelessness, are major priorities for the VHA and VBA.19 The VA Home Loan Program may represent an important resource to help veterans achieve long-term housing stability through home ownership. There has been wide public concern about housing affordability and the ability of many Americans, including veterans, to achieve home ownership.20 Homeownership is considered an important part of developing financial assets and achieving financial stability. Lowincome veterans, in particular, may benefit from this program as a national study found that 8.0% of low-income veterans and 13.9% of veterans with a history of homelessness have previously experienced a home foreclosure. 21 A greater understanding of who applies for and receives assistance from the VA Home Loan Program would inform homelessness prevention services and future planning for this program.

We conducted a quality improvement (QI) project on behalf of the VHA Homeless Programs Office and in partnership with the VBA. Our goals were to: (1) describe the annual number of applicants and recipients of the VA Home Loan Program by age group, sex, race/ethnicity, presence of any diagnosed substance use and/or mental health disorder, and history of homelessness; and (2) compare demographic, clinical, and homelessness characteristics among individuals who apply and are granted a loan through this program, individuals who apply and are denied a loan through this program, and individuals who do not apply for a loan through this program.

Methods

This project involved linked VA administrative national databases and was undertaken by the VHA Homeless Programs Office in partnership with the VBA. Specifically, VHA and VBA databases were linked together using veteran identifiers and all data were managed and analyzed on secure VA servers. The project followed VA’s Program Guide 1200.21 for nonresearch activities and institutional review board approval was waived through sponsorship by the VA Homeless Programs Office. The VHA Corporate Data Warehouse (CDW) was accessed to obtain data from the Homeless Operations Management and Evaluation System (HOMES) and other clinical data systems used by VHA clinicians and administrators that capture diagnoses, workload, and other health care data.22,23 HOMES collects intake, progress, and outcome data on homeless veterans within its care system that enables the VA to assess the effectiveness of programs and strategically allocate resources to prevent homelessness.24,25

A list of veterans who filed disability compensation and pension claims was obtained from the VBA Office of Performance Analysis and Integrity, including Social Security number, name, city and state, date of claim submission, grant or increase in benefits, homeless status, VA home loan approval, and homeless aid for dependent children from fiscal year (FY) 2022 through FY 2024. VBA data were linked to VHA CDW electronic health record data from veterans who sought VA health care services and HOMES data on veteran participation in homeless programs who were also experiencing homelessness. VHA data included demographic characteristics (eg, sex, age, race, marital status, combat service) at an index date (earliest visit to the VHA between October 1, 2021, and September 30, 2024); military sexual trauma; clinical characteristics within 12 months prior to the index date (VHA disability rating, substance use disorder [SUD] diagnosis, mental health disorder diagnosis, Charlson Comorbidity Index [CCI] score), and homelessness experience ≤ 5 years prior to the index date.

History of homelessness ≤ 5 years prior to the index date was determined using an operational definition of homelessness based on multiple indicators, including International Classification of Diseases, Tenth Revision, Clinical Modification (ICD-10-CM) diagnostic code Z59.0; clinic stop codes or HOMES records indicating VA homeless programs clinical encounters; or a positive screen on an annual homelessness screener.16 US Department of Housing and Urban Development-VA Supportive Housing enrollees were excluded because they are considered to no longer be experiencing homelessness, and Veterans Justice Program enrollees were excluded because the program primarily focuses on serving criminal justice-involved veterans. The CCI predicts the risk of death ≤ 1 year by assessing the number and severity of a patient’s coexisting health conditions and is a valuable tool for understanding a patient’s overall health burden, aiding in clinical decision-making and evaluation research studies.26-29 Diagnoses based on ICD-10-CM codes were used to determine SUDs, mental health disorders, and CCI score, using methods that have been described in other publications.30

Population

The VBA cohort of veterans requesting benefits was further restricted to those who met the following eligibility criteria: (1) requested VA benefits FYs 2022 to 2024; (2) sought VHA services ≥ 1 time between FY 2022 and 2024; (3) had matching VBA/VHA records; (4) had no missing data on claim status and/ or demographic, clinical, and homelessness characteristics; and (5) had known home loan status FYs 2022 to 2024. The original VBA dataset consisted of 4,219,755 records and the original VHA dataset consisted of 7,170,199 records (Figure 1). The final linked VBA/VHA dataset after excluding 29 records with missing data on sex, 7 with missing data on age, 6 with missing data on marital status, and an additional 143,444 with unknown VBA claim status, consisted of 3,089,295 records corresponding to 2,260,851 unique veterans. Specifically, 251,796 records corresponded to veterans who had applied and received a loan, 84,751 to veterans who had applied and were nonrecipients of a loan, and 2,752,748 to veterans who did not apply for a loan.

Abbreviations: FY, fiscal year; VBA, Veterans Benefits Administration; VHA, Veterans Health Administration.

Statistical Analysis

All statistical analyses were performed using SAS Enterprise Guide, an application that provides a point-and-click interface for data access, analysis, and management, accommodating both code-based and visual programming. 31 First, we relied on the final analytic sample to calculate the annual proportions of veterans who applied for and/or received a loan through the VA Home Loan Program. We also generated descriptive statistics stratified by age group, sex, race/ethnicity, SUD, mental health disorder, and homelessness, overall and within each FY. Pearson χ2 and Cochran-Armitage trend tests were applied to examine differences in application and receipt of a home loan by baseline characteristics and FY, respectively. Second, we conducted bivariate and multivariable analyses to compare demographic, clinical, and homelessness characteristics between 3 groups of veterans as they pertain to the VA Home Loan Program. Veterans who applied and were nonrecipients of a loan (group 1), veterans who applied and were recipients of a loan (group 2), and veterans who did not apply for a loan (group 3). Similar analyses compared VA Home Loan Program applicants who were recipients of a home loan vs VA Home Loan Program applicants who were nonrecipients of a home loan. Multinomial and binary logistic regression models were constructed to estimate the relative risk ratio (RR) and odds ratio (OR) with 95% CIs for comparisons between these distinct groups on demographic, clinical, and homelessness characteristics. Two-sided statistical tests were evaluated at α = 0.05.

Results

Tables 1 and 2 present the number of VBA applicants, including those who applied for and received benefits through the VA Home Loan Program, by age group, sex, race/ethnicity, as well as histories of SUDs, mental health disorders, and homelessness, overall, and by FY. As shown in Figure 2, 336,547 of 3,089,295 VBA applications (10.9%) pertained to the VA Home Loan Program, with a statistically significant decline in application rates, from 12.2% in FY 2022 to 9.9% in FY 2024 (P < .001 for trend). Among 336,547 veterans who applied for the VA Home Loan Program, 251,796 (74.8%) received a home loan during FYs 2022 to 2024, ranging between 73.8% for FY 2024 and 75.5% for FY 2023 (P < .001 for trend).

Veterans Affairs Home Loan Program, fiscal years (FY) 2022-2024.

Multinomial logistic regression models for demographic, clinical, and homelessness characteristics as predictors of VA Home Loan Program status are provided in Appendix 1. Based on the fully adjusted model, compared with veterans who did not apply to the VA Home Loan Program, those who applied for a home loan were less likely to be aged ≥ 50 years, unmarried, Hispanic ethnicity, mixed race, or other race, diagnosed with a SUD, or history of homelessness. Veterans with higher VA service-connected disability ratings were more frequently recipients of VA home loans, whereas those who self-identified as non-Hispanic Black and those with higher CCI scores were less frequently recipients of VA home loans. Finally, those with mental health disorders were more likely than their counterparts to be applicants (recipients or nonrecipients) of VA home loans.

Binary logistic regression models for demographic, clinical, and homelessness characteristics as predictors of receipt status among applicants to the VA Home Loan Program are provided in Appendix 2. Among applicants, those who were granted a VA home loan were less likely to be aged ≥ 50 years; have a CCI score > 0; have experienced combat service and/or military sexual trauma; be diagnosed with a SUD and/or mental health disorder; or to have a history of homelessness compared with those denied a VA home loan. Applicants granted a VA home loan were also more likely to be female, non-Hispanic White, single or never married, and/or have a VA service-connected disability ratings > 0%.

Discussion

The VA Home Loan Program is a unique benefit and resource for eligible veterans that may be increasingly important in a time of growing concern about the affordability of housing for many Americans. Research on other federally-supported home loan programs as well as private home mortgage programs has been mostly conducted in the economic realm, and studies focused on understanding these programs from a health care system perspective have been sparse.32,33 However, there is a large body of literature documenting the importance of stable, safe, and secure housing on health and well-being.34-37 This study did not focus on evaluating the effects of the VA Home Loan Program, because we wanted to first examine the characteristics of veterans who benefited from the program and how they differed from veterans who did not apply or did apply but had a denied application.

Our findings suggest that several thousands of veterans benefit from the VA Home Loan Program each year. For historical context, the time period examined was one of economic downturn with rising costs of living, including housing, and steady increases in homelessness as reported in the annual point-in-time count of sheltered and unsheltered people experiencing homelessness on a single night as mandated by the US Department of Housing and Urban Development.38-40 The Sergeant First Class Heath Robinson Honoring Our Promise to Address Comprehensive Toxics (PACT) Act of 2022 expanded health care and benefits for veterans exposed to burn pits, Agent Orange, and other toxic substances, resulting in more VA disability benefit claims, including large retroactive payments.41-43 Anecdotally, the VBA has noted that the PACT Act helped some homeless veterans with funds and stability to exit homelessness and enroll in the VA Home Loan Program.

Our analysis suggests that beneficiaries of the VA Home Loan Program were frequently aged < 50 years, female, of non-Hispanic White race, and did not have histories of psychiatric disorders or homelessness. Most of these demographic and clinical characteristics were not surprising given the composition of the veteran population, although in-depth analyses are needed to examine sex differences that may have led to more females than males benefiting from the VA Home Loan Program. In addition, it was notable that many younger and non-Hispanic Black veterans had applied. While relatively few veterans with SUDs benefited from the VA Home Loan Program, few had applied. Research is warranted into why veterans with SUDs are less likely to apply for home loans. Quite surprisingly, a sizable proportion of veterans with histories of homelessness reported they had applied to the VA Home Loan Program, although they were less likely than veterans who had not experienced homelessness to be granted a loan.

The examination of differences between veterans who did not apply, were granted, and denied a loan through the VA Home Loan Program revealed several key predictors of application outcomes in multivariable models. Specifically, veterans who applied for home loans were less likely to be aged ≥ 50 years, unmarried, of Hispanic, mixed, or other race/ethnicity, diagnosed with an SUD, or have a history of homelessness. Veterans with higher disability ratings were less frequently denied and more frequently approved, while non-Hispanic Black veterans and those with higher CCI scores were more frequently denied and less frequently approved. VBA applicants with mental health disorders were also more likely to apply for a home loan. Conversely, those granted a home loan were more likely than those denied a home loan to be female, non-Hispanic White, single/unmarried, or to have > 0% VA service-connected disability rating, but less likely to be aged ≥ 50 years, have CCI score > 0, be diagnosed with psychiatric disorders, or have a history of homelessness.

Limitations

This analysis was restricted to a subset of FY 2022 to FY 2024 linked VBA/VHA databases (ie, to veterans who had both VBA and VHA records and met prespecified eligibility criteria). Despite the large number of linked records, a small percentage of these records corresponded to veterans who were applicants or recipients of the VA Home Loan Program. Future studies should expand the time frame to examine variations in application outcomes over time and by background characteristics of veterans enrolled in VHA care who applied for VBA benefits. In addition, we relied on data and ICD-10-CM diagnostic codes from existing electronic health records and claims data to define histories of homelessness, comorbidities, SUDs, and mental health disorders. Given the time-varying nature of these conditions, the temporal sequence of events was difficult to ascertain. Third, it is worth noting that these findings can only be generalized to veterans who applied for VBA benefits and met eligibility criteria, and that these veterans may differ in terms of their demographic and clinical characteristics from those who did not apply for these benefits.

Conclusions

This study analyzed data from 251,796 individuals who applied for and received a VA home loan, 84,751 who were denied a VA home loan, and 2,752,748 veterans who did not apply for a VA home loan from FY 2022 to FY 2024. Accordingly, 11% of applications pertained to the VA Home Loan Program, and 75% of VA Home Loan Program applicants received a home loan. Distinct demographic and clinical characteristics were observed for applicants and recipients of the VA Home Loan Program, which can set the stage for future planning and evaluation of the program. Despite the broad accessibility of veterans to the VA Home Loan Program, there were differences in approval rates among applicants based on sociodemographic and clinical characteristics. Further evaluation, perhaps using qualitative methods, is needed to better understand opportunities and challenges to achieving a VA home loan, especially among underserved veteran populations. Investigation and research can guide future recommendations for any development or corrective actions that can help increase access to veterans who can benefit from the program. Future analyses are also needed to compare veterans enrolled and not enrolled in the VA Home Loan Program on health care-related outcomes.

- US Department of Veterans Affairs. Home loans. Accessed April 1, 2026. https://www.benefits.va.gov/homeloans/

- Veterans United Home Loans. VA loans: the complete guide. Accessed April 1, 2026. https://www.veteransunited.com/va-loans/

- US Department of Veterans Affairs. VA-backed veterans home loans. Accessed April 1, 2026. https://www.va.gov/housing-assistance/home-loans/

- Choplin JM, Stark DP. Whispering sweet nothings: a review of verbal behaviors that undermine the effectiveness of government-mandated home-loan disclosures. Cogn Res Princ Implic. 2019;4:6. doi:10.1186/s41235-019-0154-7

- Evans M. Borrowing boon. More explore federal home loan banks backing. Mod Healthc. 2009;39:14.

- Hogarth M. A home loan: how—and how much? Nurs Times. 1973;69:908-909.

- Jacoby SF. Home Owners’ Loan Corporation maps and place-based injury risks: a complex history. Am J Public Health. 2023;113:356-358. doi:10.2105/AJPH.2023.307242

- Merrell C. Finance. Home: a loan. Nurs Times. 1996;92:61-64.

- Namin S, Xu W, Zhou Y, et al. The legacy of the Home Owners’ Loan Corporation and the political ecology of urban trees and air pollution in the United States. Soc Sci Med. 2020;246:112758. doi:10.1016/j.socscimed.2019.112758

- Namin S, Zhou Y, Xu W, et al. Persistence of mortgage lending bias in the United States: 80 years after the Home Owners’ Loan Corporation security maps. J Race Ethn City. 2022;3:70-94. doi:10.1080/26884674.2021.2019568

- Slottow R. The home loan program. J Natl Assoc Hosp Dev. 1990:43-45.

- Wang M, Chen H, Wang L. Locus of control and home mortgage loan behaviour. Int J Psychol. 2008;43:125-129. doi:10.1080/00207590801888760

- US Dept of Veterans Affairs. Veterans Health Administration. About VHA. Updated January 20, 2025. Accessed April 1, 2026. https://www.va.gov/health/aboutvha.asp

- US Dept of Veterans Affairs. VA homeless programs. Updated May 7, 2026. Accessed May 8, 2026. https://department.va.gov/homeless/

- DiTosto JD, Holder K, Soyemi E, et al. Housing instability and adverse perinatal outcomes: a systematic review. Am J Obstet Gynecol MFM. 2021;3:100477. doi:10.1016/j.ajogmf.2021.100477

- Tsai J, Szymkowiak D, Jutkowitz E. Developing an operational definition of housing instability and homelessness in Veterans Health Administration medical records. PLoS One. 2022;17:e0279973. doi:10.1371/journal.pone.0279973

- Fowler PJ, Hovmand PS, Marcal KE, et al. Solving homelessness from a complex systems perspective: insights for prevention responses. Annu Rev Public Health. 2019;40: 465-486. doi:10.1146/annurev-publhealth-040617-013553

- US Department of Health and Human Services. Healthy People 2030: housing instability. Accessed April 1, 2026. https://health.gov/healthypeople/priority-areas/social-determinants-health/literature-summaries/housing-instability

- US Department of Veterans Affairs. VA health care priorities. Accessed April 1, 2026. https://www.va.gov/health/priorities/index.asp

- Tsai J. Federal priorities to address homelessness as a community health problem. Fam Community Health. 2025;48:57-69.

- Tsai J, Hooshyar D. Prevalence of eviction, home foreclosure, and homelessness among low-income US veterans: the National Veteran Homeless and Other Poverty Experiences study. Public Health. 2022;213:181-188. doi:10.1016/j.puhe.2022.10.017

- US Department of Veterans Affairs. Corporate Data Warehouse (CDW). Accessed April 1, 2026. https://www.hsrd.research.va.gov/for_researchers/cdw.cfm

- Price LE, Shea K, Gephart S. The Veterans Affairs Corporate Data Warehouse: uses and implications for nursing research and practice. Nurs Adm Q. 2015;39:311-318. doi:10.1097/NAQ.0000000000000118

- US Department of Veterans Affairs. Homeless Operations Management and Evaluation System (HOMES) User Manual—Phase 1. April 19, 2011. Accessed April 1, 2026. https://www.adldata.org/wp-content/uploads/2016/07/homes.pdf

- Tsai J, Kasprow WJ, Rosenheck RA. Latent homeless risk profiles of a national sample of homeless veterans and their relation to program referral and admission patterns. Am J Public Health. 2013;103:S239-S247. doi:10.2105/AJPH.2013.301322

- Sundararajan V, Henderson T, Perry C, et al. New ICD-10 version of the Charlson comorbidity index predicted inhospital mortality. J Clin Epidemiol. 2004;57:1288-1294. doi:10.1016/j.jclinepi.2004.03.012

- Beydoun HA, Szymkowiak D, Beydoun MA, et al. Comparing major comorbidity indices as predictors of all-cause mortality in the Veterans Affairs health care system. J Clin Epidemiol. 2025;182:111778. doi:10.1016/j.jclinepi.2025.111778

- Charlson ME, Carrozzino D, Guidi J, et al. Charlson Comorbidity Index: a critical review of clinimetric properties. Psychother Psychosom. 2022;91:8-35. doi:10.1159/000521288

- Glasheen WP, Cordier T, Gumpina R, et al. Charlson Comorbidity Index: ICD-9 update and ICD-10 translation. Am Health Drug Benefits. 2019;12:188-197.

- Beydoun HA, Szymkowiak D, Kinney R, et al. Is the risk of Alzheimer’s disease and related dementias among US veterans influenced by the intersectionality of housing status, HIV/AIDS, hepatitis C, and psychiatric disorders? J Gerontol A Biol Sci Med Sci. 2024;79:glae153. doi:10.1093/gerona/glae153

- SAS Institute. SAS Enterprise Guide. Accessed April 1, 2026. https://www.sas.com/en_us/software/enterprise-guide/features-list.html

- Agarwal S, Amromin G, Chomsisengphet S, et al. Mortgage refinancing, consumer spending, and competition: evidence from the Home Affordable Refinance Program. Rev Econ Stud. 2023;90:499-537.

- Ashcraft A, Bech ML, Frame WS. The Federal Home Loan Bank System: the lender of next-to-last resort? J Money Credit Bank. 2010;42:551-583.

- Gibson M, Petticrew M, Bambra C, et al. Housing and health inequalities: a synthesis of systematic reviews of interventions aimed at different pathways linking housing and health. Health Place. 2011;17:175-184. doi:10.1016/j.healthplace.2010.09.011

- Shaw M. Housing and public health. Annu Rev Public Health. 2004; 25:397-418. doi:10.1146/annurev.publhealth.25.101802.123036

- Thomson H, Petticrew M, Morrison D. Health effects of housing improvement: systematic review of intervention studies. BMJ. 2001;323:187-190. doi:10.1136/bmj.323.7306.187

- Tsai J. Theorizing pathways between eviction filings and increased mortality risk. JAMA. 2024;331:570-571. doi:10.1001/jama.2023.27978

- Bernanke B, Blanchard O. What caused the US pandemicera inflation? Am Econ J Macroecon. 2025;17:1-35.

- Hall SG, Tavlas GS, Wang Y. Drivers and spillover effects of inflation: the United States, the euro area, and the United Kingdom. J Int Money Finance. 2023;131:1-13.

- US Department of Housing and Urban Development. Point-in-Time Count and Housing Inventory Count. Accessed April 1, 2026. https://www.hudexchange.info/programs/hdx/pit-hic/

- Beckman AL, Jacobs J, Elnahal SM. The PACT Act: expanding coverage and access for veterans. JAMA. 2024;332:1423-1424. doi:10.1001/jama.2024.16013

- Zychowicz ME. The PACT Act: enhancing health care access for military personnel and veterans. N C Med J. 2023;84:379-380. doi:10.18043/001c.89208

- US Department of Veterans Affairs. The PACT Act and your VA benefits. April 2, 2026. https://www.va.gov/resources/the-pact-act-and-your-va-benefits/

- US Department of Veterans Affairs. Home loans. Accessed April 1, 2026. https://www.benefits.va.gov/homeloans/

- Veterans United Home Loans. VA loans: the complete guide. Accessed April 1, 2026. https://www.veteransunited.com/va-loans/

- US Department of Veterans Affairs. VA-backed veterans home loans. Accessed April 1, 2026. https://www.va.gov/housing-assistance/home-loans/

- Choplin JM, Stark DP. Whispering sweet nothings: a review of verbal behaviors that undermine the effectiveness of government-mandated home-loan disclosures. Cogn Res Princ Implic. 2019;4:6. doi:10.1186/s41235-019-0154-7

- Evans M. Borrowing boon. More explore federal home loan banks backing. Mod Healthc. 2009;39:14.

- Hogarth M. A home loan: how—and how much? Nurs Times. 1973;69:908-909.

- Jacoby SF. Home Owners’ Loan Corporation maps and place-based injury risks: a complex history. Am J Public Health. 2023;113:356-358. doi:10.2105/AJPH.2023.307242

- Merrell C. Finance. Home: a loan. Nurs Times. 1996;92:61-64.

- Namin S, Xu W, Zhou Y, et al. The legacy of the Home Owners’ Loan Corporation and the political ecology of urban trees and air pollution in the United States. Soc Sci Med. 2020;246:112758. doi:10.1016/j.socscimed.2019.112758

- Namin S, Zhou Y, Xu W, et al. Persistence of mortgage lending bias in the United States: 80 years after the Home Owners’ Loan Corporation security maps. J Race Ethn City. 2022;3:70-94. doi:10.1080/26884674.2021.2019568

- Slottow R. The home loan program. J Natl Assoc Hosp Dev. 1990:43-45.

- Wang M, Chen H, Wang L. Locus of control and home mortgage loan behaviour. Int J Psychol. 2008;43:125-129. doi:10.1080/00207590801888760

- US Dept of Veterans Affairs. Veterans Health Administration. About VHA. Updated January 20, 2025. Accessed April 1, 2026. https://www.va.gov/health/aboutvha.asp

- US Dept of Veterans Affairs. VA homeless programs. Updated May 7, 2026. Accessed May 8, 2026. https://department.va.gov/homeless/

- DiTosto JD, Holder K, Soyemi E, et al. Housing instability and adverse perinatal outcomes: a systematic review. Am J Obstet Gynecol MFM. 2021;3:100477. doi:10.1016/j.ajogmf.2021.100477

- Tsai J, Szymkowiak D, Jutkowitz E. Developing an operational definition of housing instability and homelessness in Veterans Health Administration medical records. PLoS One. 2022;17:e0279973. doi:10.1371/journal.pone.0279973

- Fowler PJ, Hovmand PS, Marcal KE, et al. Solving homelessness from a complex systems perspective: insights for prevention responses. Annu Rev Public Health. 2019;40: 465-486. doi:10.1146/annurev-publhealth-040617-013553

- US Department of Health and Human Services. Healthy People 2030: housing instability. Accessed April 1, 2026. https://health.gov/healthypeople/priority-areas/social-determinants-health/literature-summaries/housing-instability

- US Department of Veterans Affairs. VA health care priorities. Accessed April 1, 2026. https://www.va.gov/health/priorities/index.asp

- Tsai J. Federal priorities to address homelessness as a community health problem. Fam Community Health. 2025;48:57-69.

- Tsai J, Hooshyar D. Prevalence of eviction, home foreclosure, and homelessness among low-income US veterans: the National Veteran Homeless and Other Poverty Experiences study. Public Health. 2022;213:181-188. doi:10.1016/j.puhe.2022.10.017

- US Department of Veterans Affairs. Corporate Data Warehouse (CDW). Accessed April 1, 2026. https://www.hsrd.research.va.gov/for_researchers/cdw.cfm

- Price LE, Shea K, Gephart S. The Veterans Affairs Corporate Data Warehouse: uses and implications for nursing research and practice. Nurs Adm Q. 2015;39:311-318. doi:10.1097/NAQ.0000000000000118

- US Department of Veterans Affairs. Homeless Operations Management and Evaluation System (HOMES) User Manual—Phase 1. April 19, 2011. Accessed April 1, 2026. https://www.adldata.org/wp-content/uploads/2016/07/homes.pdf

- Tsai J, Kasprow WJ, Rosenheck RA. Latent homeless risk profiles of a national sample of homeless veterans and their relation to program referral and admission patterns. Am J Public Health. 2013;103:S239-S247. doi:10.2105/AJPH.2013.301322

- Sundararajan V, Henderson T, Perry C, et al. New ICD-10 version of the Charlson comorbidity index predicted inhospital mortality. J Clin Epidemiol. 2004;57:1288-1294. doi:10.1016/j.jclinepi.2004.03.012

- Beydoun HA, Szymkowiak D, Beydoun MA, et al. Comparing major comorbidity indices as predictors of all-cause mortality in the Veterans Affairs health care system. J Clin Epidemiol. 2025;182:111778. doi:10.1016/j.jclinepi.2025.111778

- Charlson ME, Carrozzino D, Guidi J, et al. Charlson Comorbidity Index: a critical review of clinimetric properties. Psychother Psychosom. 2022;91:8-35. doi:10.1159/000521288

- Glasheen WP, Cordier T, Gumpina R, et al. Charlson Comorbidity Index: ICD-9 update and ICD-10 translation. Am Health Drug Benefits. 2019;12:188-197.

- Beydoun HA, Szymkowiak D, Kinney R, et al. Is the risk of Alzheimer’s disease and related dementias among US veterans influenced by the intersectionality of housing status, HIV/AIDS, hepatitis C, and psychiatric disorders? J Gerontol A Biol Sci Med Sci. 2024;79:glae153. doi:10.1093/gerona/glae153

- SAS Institute. SAS Enterprise Guide. Accessed April 1, 2026. https://www.sas.com/en_us/software/enterprise-guide/features-list.html